MCAI Lex Vision: Compass Transaction Fees Convert a Private-Listing Dispute Into a State AG Platform-Control Case

A $475 Fee, a C-Suite Skillman Moment, and the State AG Platform-Control Bridge

Related works: Why Compass Needs Private Listings, The Inventory-Routing Premium — Compass, the Anywhere Merger, and the Multi-State Enforcement Window | Compass’s Interpretation of “Public Marketing” May Draw Antitrust Scrutiny from State Attorneys General | Compass’s Skillman Moment Reaches the C-Suite, Cris Nelson Moment Holds at the Regional Tier

I. Vision Statement

Compass’s transaction-fee litigation reframes the state attorney general analysis. The Florida class action hands enforcers a document-backed consumer-harm theory that reaches past private listings into the closing table — a $475 buyer-paid charge written into a purchase contract and collected at closing. A separate Illinois case supplies parallel doctrine without deciding the Florida fee: in Batton v. Compass, the homebuyer-commission antitrust action, Judge LaShonda Hunt’s March 24, 2026 order (N.D. Ill.) carried buyer-side claims against Compass and four other brokerages past a motion to dismiss, and her reasoning helps explain why a document-backed transaction-fee theory may prove more durable than a buyer-side commission theory.

Private exclusives raised the first question: whether Compass can shape market visibility by controlling when inventory reaches public channels. Transaction fees raise the second: whether Compass can convert a scaled brokerage platform into a fee-imposition system that monetizes consumers through standardized charges embedded inside the transaction workflow.

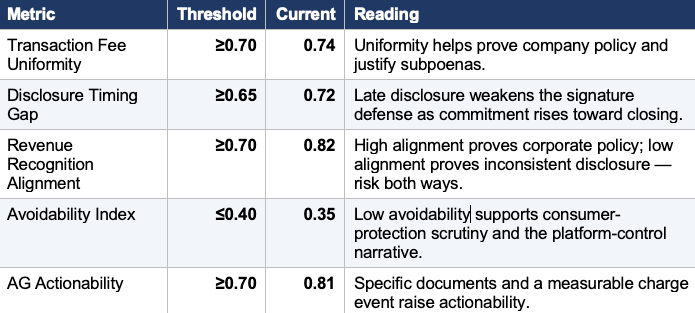

A $475 fee creates no antitrust violation standing alone. The fee gains legal and strategic weight because Compass reportedly treats flat transaction commission fees as a revenue stream, while the Florida complaint alleges Compass inserted the charge into a Florida Realtors/Florida Bar purchase contract and collected it at closing. The complaint attaches the purchase contract and settlement statement, showing a $475 buyer-paid “Flat transaction commission” and a separate closing-line “Transaction Fee to Compass Florida LLC,” alongside a $6,000 selling-agent commission to Compass Florida LLC.

A Skillman Moment, in the MindCast framework, is a category error: a Compass actor reframes a public market-design or regulatory question as a private matter of seller or buyer choice. The term traces to Compass broker Moya Skillman, who, asked about Washington’s law restricting pocket listings (SSB 6091), told the Puget Sound Business Journal that sellers should decide how and when to market their homes — applying brokerage choice messaging to a state licensing statute and collapsing a market-transparency rule into private preference. Compass repeats the error at the corporate tier when it recognizes the transaction fee in SEC filings and defends it publicly as routine and disclosed, answering a consumer-protection and market-structure question with private business custom. Broker Skillman made the move at the regional tier; the securities filing and corporate messaging make it at the C-suite, the escalation traced in the MindCast: Skillman Moment Reaches the C-Suite. The rest of this paper follows the consequence: a fee owned and defended at the top tier gives attorneys general a document-backed bridge from private-listing transparency to platform-control enforcement.

State AGs should treat the transaction-fee issue as a platform-control signal, not a junk-fee dispute. Compass’s own platform manages the deal from first contact to close, spanning pre-public inventory, agent routing, buyer access, referral economics, standardized workflow software, integrated title and escrow, and closing-table extraction — the control architecture MindCast has tracked across the MindCast: Commission Consolidation Strategy and the MindCast: Letter to State Attorneys General. The operative enforcement question becomes whether Compass’s scale lets the company impose charges and transaction terms that ordinary brokerage competition would otherwise discipline. Batton (Section VI) then explains why state attorneys general, rather than private buyer classes, may hold the strongest vector to test that question.

II. Core Thesis

Compass’s legal exposure no longer turns only on whether private listings distort MLS transparency. Transaction-fee litigation adds a closing-table extraction layer to the same market-structure story.

Compass can argue that buyers signed the contract and closing statement. Signature helps Compass on disclosure, but signature does not resolve the broader enforcement question. State AGs can ask whether Compass converted brokerage scale, post-merger integration, and transaction-management infrastructure into a fee-imposition system that consumers encounter only after they have already committed to a home purchase.

The antitrust theory should not claim “$475 equals monopoly conduct.” As the MindCast: Chicago School — Coaseanalysis frames it, the fee matters because it exposes who controls the transaction architecture, not because $475 alone proves harm. The stronger theory asks whether Compass’s consolidated platform lets the company control inventory access, route consumers, standardize fee practices, and extract transaction revenue across multiple points in the deal lifecycle — the revenue-architecture pattern set out in the MindCast: Cybernetics of Compass’s Narrative Control.

III. Florida Complaint: Why the Documents Matter

The Florida class action gives regulators a clean evidentiary starting point. Plaintiffs allege Compass Florida represented buyers, used a Florida Realtors/Florida Bar “AS IS” Residential Contract for Sale and Purchase, added a buyer-paid $475 flat transaction commission into the “Additional Terms” section, and later collected the same amount at closing.

The complaint carries unusual enforcement value because the exhibits reduce abstraction. The purchase contract shows the fee language. The ALTA settlement statement shows the fee collection. The same closing statement also shows Compass Florida LLC received a $6,000 selling-agent commission. Plaintiffs can therefore argue Compass received seller-side compensation and imposed an additional buyer-side charge through the transaction documents.

Consumer-protection claims provide the strongest immediate pathway. The Florida Deceptive and Unfair Trade Practices Act theory targets the business practice directly: charging buyers a fee allegedly not incurred, not supported by performed services, unreasonable, excessive, or not owed. The Florida Consumer Collection Practices Act claim carries more risk because Compass will argue the signed contract created a payment right, but the claim still supplies discovery leverage over fee legitimacy, collection knowledge, and company policy.

IV. SEC Revenue Disclosure Changes the Risk Profile

Compass’s SEC disclosure changes the litigation and AG posture because it undercuts the “rogue agent” frame. A company-level revenue disclosure that recognizes “flat transaction commission fees” within owned-brokerage revenue lets plaintiffs and AGs argue Compass did not merely tolerate scattered local charges. Compass recognized the fee category as part of its owned-brokerage revenue model.

The same disclosure also stages a category error. When Compass recognizes the fee in filings and then defends it publicly as routine, disclosed, standard practice, it answers a consumer-protection and market-structure question with private business custom — the Skillman Moment reaching the C-suite. Broker Moya Skillman applied seller-choice messaging to a state licensing statute; Compass now applies standard-practice messaging to a fee that raises market-transparency and platform-control questions. The MindCast: Self-Disclosure Trap shows the documents that make the error legible; the MindCast: Skillman Moment Reaches the C-Suite traces it from the regional tier to corporate leadership; and corporate recognition of the fee undercuts any later attempt to recast the charge as stray agent conduct.

Recognizing the fee as company revenue does not prove unlawful conduct, but it reframes discovery and sharpens the cross-forum exposure traced in the MindCast: Strategic Antitrust Forum Shopping and the MindCast: Self-Disclosure Trap: Compass cannot easily tell investors the fee is a revenue line while telling courts it is incidental or agent-level. The central question no longer asks whether one agent added a fee. It asks how Compass operationalized, disclosed, documented, routed, collected, and accounted for transaction-fee revenue.

State AG subpoenas could target state-by-state fee schedules, rollout and standardization records, post-Anywhere integration documents, agent scripts, compliance guidance, template purchase-agreement language, platform fields that auto-populate fees, escrow or title closing instructions, revenue accounting codes, consumer complaints, refund data, waiver practices, and legal-risk reviews.

V. Broader Class Action Risk

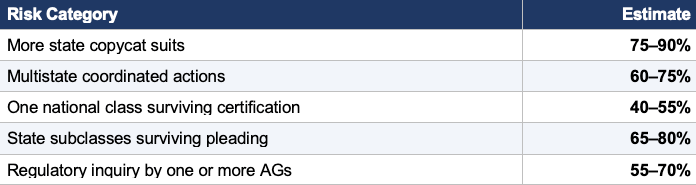

Broader class-action risk looks high, although plaintiffs will likely proceed state by state rather than through one clean national class. Different state forms, brokerage-agreement rules, consumer-protection statutes, disclosure regimes, arbitration provisions, and buyer-broker practices create certification problems for one nationwide class.

State copycat suits look more plausible. Plaintiffs’ firms can use the Florida complaint as a template: identify Compass buyer transactions, obtain purchase contracts and settlement statements, isolate the transaction-fee line, compare fee timing against buyer-broker disclosures, and plead unfair or deceptive fee collection under state law.

Updated risk bands remain:

High-risk states include Florida, California, New York, New Jersey, Massachusetts, Washington, Connecticut, Illinois, and Texas. Strong consumer-protection statutes, high Compass transaction volume, standardized forms, and existing scrutiny of Compass’s private-listing strategy increase risk in those markets. Washington exposure is tracked separately in the MindCast: SSB 6091 Enforcement and MindCast: Compass Plan B analyses, which test whether fee, referral, and routing channels rebuild value as transparency statutes close private-listing windows.

VI. The Batton Order: Doctrinal Supply and Current Posture

The uploaded ruling is the Batton 2 order — the buyer-side commission case naming Compass, eXp World Holdings, Redfin, Weichert, and United Real Estate — distinct from the Batton 1 track that named NAR, Anywhere, RE/MAX, and Keller Williams (Judge LaShonda A. Hunt, N.D. Ill., Case No. 1:23-cv-15618, Memorandum Opinion and Order entered March 24, 2026). One caveat governs every use of the order, so it belongs at the front: Batton litigates buyer-agent commissions, not the $475 transaction fee, and it decides nothing about the fee. The order matters because it shows which buyer-side theories survive pleading, which fail for lack of plaintiff-specific deception, and why AG enforcement can carry claims private buyer classes cannot. Read it as persuasive parallel reasoning available to either side, not controlling authority; it runs net favorable to plaintiffs on the documentary-record distinction.

The case survived and narrowed at once, every ruling fixed at the Rule 12 plausibility floor. The court dismissed without prejudice the Sherman Act § 1 injunctive-relief count — homebuyers lack antitrust standing because sellers sit better positioned — along with the Florida, Missouri, and Tennessee antitrust claims, the Colorado, Kansas, Pennsylvania, and Tennessee consumer-protection claims, and the Connecticut, Maryland, Utah, and New Hampshire antitrust claims only insofar as they predate each state’s Illinois Brick repealer. It denied dismissal of the core state antitrust conspiracy claims, denied every personal-jurisdiction challenge, rejected the statute-of-limitations defense, and denied the motion to strike class allegations — leaving the state antitrust, consumer-protection, and unjust-enrichment damages engine intact for discovery.

Two holdings carry into the MindCast framework library. Conspiracy-based personal jurisdiction, adopted from Khan v. Gramercy under the Illinois long-arm statute, anchors jurisdiction on NAR’s Illinois headquarters as the situs where the rule-promulgation agreement formed; centralized rule-making becomes the jurisdictional hook, restating Signal Suppression Equilibrium and the Nash-Stigler architecture in legal form — the centralization that manufactures coordination also manufactures forum reach. The deception-versus-pure-anticompetition split then explains the consumer-protection dismissals: the Colorado, Pennsylvania, and Kansas claims fell for want of an affirmative deceptive act tied to a named plaintiff, while the Florida, Iowa, and Virginia claims survived on the licensee-exemption fact question. An itemized $475 charge in a signed contract is the plaintiff-specific affirmative act the dismissed claims lacked.

On limitations, Batton supports the broader accrual intuition rather than supplying a borrowed doctrine. Judge Hunt applied the continuing-violation rule to state antitrust claims, holding each home purchase since December 1996 starts its own clock. Transaction-fee claims do not need that full theory — each fee collection supplies its own charge event and accrual date — so the order reinforces, without controlling, the rolling-exposure logic under the copycat bands in Section V.

The order’s least-stated insight is the one that matters most for vector selection. The court dismissed buyers’ injunctive standing because sellers are better positioned, and noted that the Illinois Antitrust Act reserves indirect-purchaser class actions to the Attorney General acting parens patriae. Private buyers face a standing ceiling and, in Illinois, a class-action bar the AG does not — doctrinal architecture that independently routes the strongest enforcement posture toward AGs, where the platform-control framing already lands.

Docket posture reframes what “survival” means in mid-2026. Keller Williams settled its Batton exposure for $20 million in February 2026; Compass and United Real Estate elected to opt into the Tuccori homebuyer settlement and moved to stay Batton pending approval, and the court denied those stays, keeping the case live. The Batton plaintiffs have challenged the Tuccori opt-in settlements as inadequate to protect homebuyer claims. A surviving motion to dismiss against Compass therefore operates as leverage against a settlement exit, not a guaranteed march toward a buyer-class trial.

Compass’s acquisition of Anywhere complicates that posture. Anywhere participated as a settling defendant in related commission litigation, and Compass closed the acquisition on January 9, 2026, so the company now carries both post-merger transaction scale and unresolved buyer-side exposure at once. Compass’s own SEC disclosure describes the Anywhere settlement’s injunctive relief, monetary relief, and remaining payment obligations — the concrete fact the platform narrative needs, with post-merger scale internalizing transaction economics and litigation resolution inside one entity.

VII. State AG Antitrust Impact

Transaction fees materially raise state AG scrutiny because they supply the consumer-harm bridge that the commission theory cannot carry — the bridge the MindCast: Why Compass Needs Private Listings — State AG Scrutiny analysis identified as the missing piece between private-inventory control and enforcement. Private listings create market-structure concern. Transaction fees create consumer-payment evidence. Together, the two move enforcers from a transparency theory to an extraction theory — and Batton explains why the extraction theory belongs in AG hands.

Judge Hunt’s March 2026 order sharpens three structural points enforcers should absorb before opening or expanding an investigation.

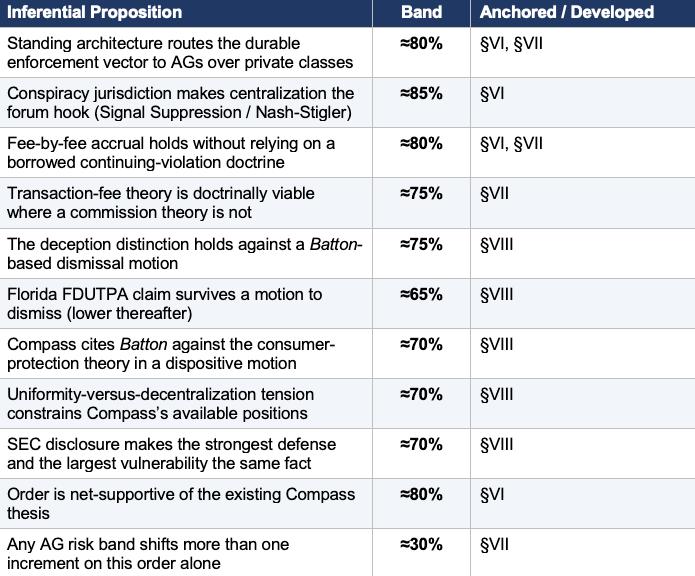

First, the standing architecture favors AGs over private classes. The court dismissed homebuyers’ injunctive standing because home sellers sit better positioned to seek that relief, and the Illinois Antitrust Act reserves indirect-purchaser class actions to the Attorney General acting parens patriae. Private buyer aggregation keeps colliding with standing ceilings and class bars that AG enforcement is designed to clear. AGs inherit the strongest posture not by rhetoric but by doctrine (≈80% that the standing structure routes the durable enforcement vector to AGs rather than private plaintiffs).

Second, repeated transaction-level injuries create rolling exposure. Judge Hunt applied the continuing-violation rule to Batton’s state antitrust claims, holding each home purchase since December 1996 starts its own limitations clock. Transaction-fee claims do not need that full doctrine: each $475 collection functions as a discrete charge event with its own accrual date, which independently blunts the statute-of-limitations defense Compass would raise against historical practice.

Third, the deception requirement separates winners from losers among consumer-protection statutes. The court dismissed the Colorado, Pennsylvania, and Kansas consumer-protection claims because plaintiffs pled anticompetitive conduct without an affirmative deceptive act tied to a named buyer. An itemized fee inserted into a signed contract and collected at closing supplies the plaintiff-specific affirmative act those statutes demand — which is why a transaction-fee theory survives where a commission theory dies (≈75%).

The standing, accrual, and deception points above let AGs frame three questions.

First, Compass may convert market power into consumer extraction. A standardized transaction fee signals pricing power when Compass controls enough agents, listings, buyer flow, or transaction infrastructure in a local market to impose a charge ordinary competition would erode.

Second, Compass may operate less like a conventional brokerage and more like a transaction platform. A platform-control theory fits when the company monetizes inventory visibility, agent workflow, referral routing, and closing-table charges across the same consolidated infrastructure.

Third, post-merger scale may produce harm rather than only efficiency. Compass can argue the Anywhere acquisition improves service and national reach. AGs can answer that integration expanded Compass’s ability to impose standardized fees, internalize transaction economics, and carry unresolved buyer-side litigation exposure inside the same post-merger entity — the merger-scrutiny posture set out in the MindCast: Letter to State Attorneys General.

The fee issue raises the probability that AGs expand existing Compass scrutiny beyond private listings. The fee issue likely does not support a standalone antitrust enforcement action without further evidence of market power or exclusionary conduct. The fee issue strongly supports broader subpoenas, consumer-protection claims, and merger-related theories about platformized brokerage control.

Updated AG risk bands:

Two bands move up one increment from prior estimates. Multistate interest rises (50–65% to 55–70%) because per-purchase accrual gives copycat plaintiffs a cleaner limitations runway, raising the suit volume that historically triggers multistate AG coordination. The broader-theory band rises (50–65% to 55–70%) because the Anywhere integration adds a concrete post-merger internalization fact to the platform narrative. The standalone-antitrust band holds, since Battons upplies no market-power or exclusionary-conduct evidence and the fee alone still does not carry a monopolization theory. Appendix A records the full register.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

VIII. Compass’s Best Defense

Compass will argue the fee appeared in signed documents, buyers authorized disbursement, and licensed agents may complete transaction forms with negotiated business terms. Compass will add that flat transaction fees reflect common brokerage practice in some markets and prove neither deception, coercion, nor market power — the “standard practice” framing the MindCast: Narrative Inversion Playbook anticipates, where control is reframed as choice and a fee as custom. Those defenses still carry real force. Disclosure and signature weaken claims that depend on concealment. State-law variation weakens nationwide certification. Agent-level variation weakens commonality and predominance.

Compass’s sharpest move will borrow Batton against the consumer-protection theory. Judge Hunt dismissed the Colorado, Pennsylvania, and Kansas consumer-protection claims because the plaintiffs pled anticompetitive conduct without an affirmative deceptive act, and Compass will frame that holding as authority that brokerage-fee practices fall outside consumer-protection statutes absent fraud. Expect the argument in exactly that compressed form.

Compass’s Batton framing fails on the facts of the dismissal. Batton rejected those claims because the buyer-agent-services-are-“free” practice was a permitted industry convention that no plaintiff alleged was misrepresented to them — an absent affirmative act, not a safe-harbor for fees. A $475 line item inserted into a signed purchase contract and collected at closing is the affirmative, plaintiff-specific act the Batton plaintiffs lacked. The distinction is not cosmetic: Batton dismissed a theory built on a non-statement, while the transaction-fee theory rests on an itemized charge that exists in the contract and the settlement statement. The cleaner the documentary record, the more the Batton citation cuts toward plaintiffs rather than Compass.

Compass will press a second, statute-specific defense unique to Florida — the FDUTPA real-estate-licensee exemption, Fla. Stat. § 501.212(6). Batton supplies the answer there too, and again in plaintiffs’ favor at the pleading stage: Judge Hunt declined to dismiss the Florida, Iowa, and Virginia consumer-protection claims because whether the licensee exemption applies is a fact question unsuitable for a motion to dismiss. The Florida transaction-fee complaint may hand Compass a stronger exemption record than the Batton pleadings gave those defendants, because the complaint’s own allegations place Compass Florida LLC and Chapter 475 licensure squarely in issue. Frame the FDUTPA point as pleading survivability rather than ultimate liability: the claim should clear a motion to dismiss, then become a discovery contest over which licensed entity charged the fee and under which statutory provision.

Compass’s defense weakens fastest if discovery surfaces centralized rollout, uniform fee amounts by state, scripted disclosures, software-driven fee insertion, standardized closing instructions, or internal recognition that consumers objected. Uniformity is the hinge. The same standardization that lets Compass defend the fee as routine industry practice also converts it from agent-level discretion into company-level policy — and company-level policy is what transforms a fee dispute into a platform-governance problem and a parens patriae target. Compass’s “standard practice” defense is itself the Skillman category error: a private-custom answer to a public market question. The company cannot claim both that the fee is too standardized to be deceptive and too decentralized to be company conduct; the defenses pull against each other.

Compass’s SEC disclosure carries the deepest exposure of all. Once Compass recognized flat transaction commission fees as a revenue category at the corporate level, the “rogue agent” frame closed, and the standardization defense Compass needs for industry-custom arguments simultaneously feeds the company-policy inference enforcers need for platform theories. Compass’s strongest factual defense and its largest structural vulnerability draw on the same fact.

IX. Enforcement Theory for State AGs

The strongest AG framing should avoid overclaiming. A precise theory would read:

Compass may have used post-merger scale and transaction-platform infrastructure to monetize multiple control points in residential brokerage, including listing visibility, agent access, referral flow, and closing-table fees. Transaction-fee evidence matters because it shows how platform control can translate into direct consumer charges after buyers enter the transaction funnel.

AGs can test the theory through documents rather than rhetoric. Enforcement staff should compare fee incidence before and after the Anywhere acquisition, measure fee uniformity by state, compare Compass fee adoption against local market share, review fee-waiver rates, identify whether fees appear first in buyer-broker agreements or later in purchase contracts, and examine whether Compass’s software or compliance workflows standardized the practice.

The enforcement question becomes empirical:

Did Compass’s scale make transaction fees easier to impose, harder for consumers to avoid, and more profitable across a consolidated brokerage network?

A yes answer strengthens antitrust scrutiny. A no answer leaves the case mostly in consumer-protection territory.

X. Public Framing

The most effective public-facing line:

Compass’s transaction-fee disclosure gives state AGs the missing consumer-harm bridge: Compass may not merely restrict listing visibility; Compass may use a scaled brokerage platform to monetize buyers and sellers through standardized charges embedded inside the transaction workflow.

A sharper AG-facing version:

Compass’s private-listing strategy controls visibility before the market sees a home. Compass’s transaction-fee practice allegedly monetizes the buyer after the transaction enters closing. Combined evidence supports inquiry into whether Compass has become a brokerage platform that extracts revenue from control points ordinary competition should constrain.

The legal record identifies the enforcement theory. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation tests how that theory is likely to move across regulators, private plaintiffs, Compass’s defenses, and public narrative pressure.

XI. Quantified Forecast: MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation

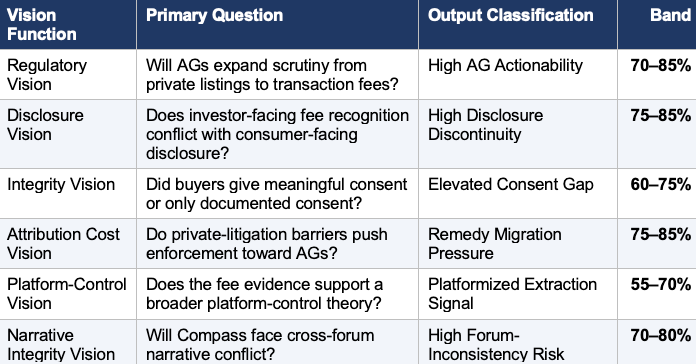

The simulation ran six Vision Functions against the Compass transaction-fee record — Regulatory Vision, Disclosure Vision, Integrity Vision, Attribution Cost Vision, Platform-Control Vision, and Narrative Integrity Vision. Each function tests a separate enforcement layer: regulator incentives, disclosure mismatch, consumer assent, private-litigation limits, platform structure, and cross-forum narrative coherence.

Simulation results converge on one finding. The $475 fee carries no standalone antitrust theory by itself; it carries enforcement value because it links a consumer injury to the broader platform-control thesis — Compass may control visibility before a home reaches the market, then monetize buyers and sellers once the transaction enters the closing workflow. The highest-confidence output is not immediate antitrust liability but investigative expansion: AGs can use the fee as a subpoena hook for fee schedules, rollout records, software fields, closing instructions, waiver data, consumer complaints, and post-Anywhere integration documents. The combined forecast lands at an 80–85% confidence band.

Simulation Input Record

The simulation used five inputs. The Florida class action alleges Compass Florida inserted a buyer-paid $475 “Flat transaction commission” into a Florida Realtors/Florida Bar purchase contract and collected the same amount on the closing statement, alongside a $6,000 selling-agent commission to Compass Florida LLC. Compass’s SEC disclosure recognizes “flat transaction commission fees” within owned-brokerage revenue, weakening the isolated-agent argument. Compass’s public platform narrative emphasizes end-to-end transaction workflow, which raises the fee’s significance when one firm manages inventory visibility, agent workflow, referrals, title or escrow adjacency, and closing economics across one path. Batton v. Compass decides nothing about the $475 fee but shows which buyer-side theories survive pleading and why AG enforcement can carry claims private buyer classes cannot. The existing MindCast Compass corpus already identified private-listing transparency harm, commission consolidation, forum-shopping risk, narrative inversion, state AG scrutiny, and post-SSB 6091 circumvention risk; transaction-fee evidence adds the missing consumer-payment layer.

Simulation Run Matrix

Regulatory Vision

Function. Regulatory Vision evaluates whether a fact pattern can move from private litigation into state attorney general investigation, measuring enforcement incentives, subpoena readiness, consumer-protection fit, antitrust adjacency, and multistate coordination potential.

Reading. The transaction fee gives AGs a cleaner opening than private listings alone. Private listings force enforcers to explain market visibility, off-MLS timing, private-inventory effects, and buyer-access distortion; the fee asks a simpler first question — did Compass impose a standardized buyer-paid charge through transaction documents while recognizing similar fees as corporate revenue? Consumer-protection authority carries the first wave; antitrust authority carries the second only if discovery connects the fee to market power, post-merger scale, or platform routing. The function predicts a document-rich gateway into broader Compass conduct, not an antitrust suit on the fee alone.

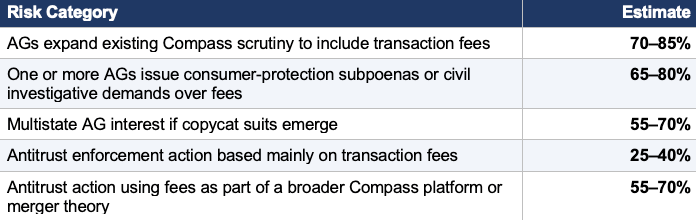

— AG expansion into transaction-fee scrutiny: 70–85% if copycat suits, press coverage, or consumer complaints continue.

— Consumer-protection subpoenas or CIDs: 65–80%, since the Florida complaint supplies a ready document-request template.

— Multistate AG interest: 55–70% if plaintiffs file copycat suits in high-volume Compass markets.

— Standalone antitrust enforcement on the fee alone: 25–40%, absent market-power, exclusionary-conduct, or coercion evidence.

— Broader antitrust scrutiny using the fee as platform-conduct evidence: 55–70%.

Disclosure Vision

Function. Disclosure Vision evaluates whether a company’s statements, documents, and transaction practices create cross-forum inconsistency, comparing investor disclosures, consumer disclosures, litigation positions, agent scripts, and regulatory narratives.

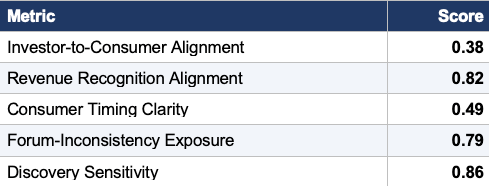

Reading. Corporate recognition of flat transaction commission fees suggests a revenue category, not a stray closing error, while the Florida complaint alleges the buyer met the $475 charge through a contract term and a settlement-statement line. Compass benefits from calling the fee revenue to investors and disclosed, routine, local, or agent-level in litigation; AGs can probe whether those descriptions cover one practice or several. Consumer timing will likely matter more than bare disclosure, since meaningful disclosure requires more than a signature when the buyer meets the charge after selecting an agent and entering the funnel.

— SEC disclosure becomes a discovery anchor: 75–85% — accounting codes, fee-recognition policies, state fee schedules, revenue reports.

— Compass argues signed contracts and closing statements gave adequate disclosure: 80–90%.

— Plaintiffs and AGs answer that timing, service basis, and standardization outweigh a line item: 70–80%.

— Forum inconsistency becomes a narrative problem: 70–80%, since revenue recognition conflicts with any minimizing litigation posture.

Integrity Vision

Function. Integrity Vision evaluates whether a transaction process preserves meaningful consumer autonomy, distinguishing documented consent from informed assent and testing whether a workflow places the firm’s economic interest above a consumer’s reasonable expectations.

Reading. Compass’s strongest defense relies on documented consent: buyers signed the contract and closing statement, and courts will not ignore signatures. The function separates signature from meaningful choice — a buyer may sign without knowing whether the fee compensates the agent, compensates the brokerage, duplicates a commission, covers a separate service, or remains negotiable. The $6,000 selling-agent commission shown beside the $475 charge sharpens the expectation conflict, since buyers may reasonably ask why a separate buyer-paid charge exists when Compass already received commission compensation.

— Compass’s signature defense carries real pleading and summary-judgment value: 60–75%.

— Plaintiffs survive initial consumer-protection screening if they frame unsupported fee extraction rather than concealment: 60–75%.

— Service-basis discovery becomes decisive: 75–85% — what service did the $475 cover that the commission did not?

— Fee avoidability becomes a major factual issue: 70–80% — could consumers reject, negotiate, waive, or avoid the fee before committing?

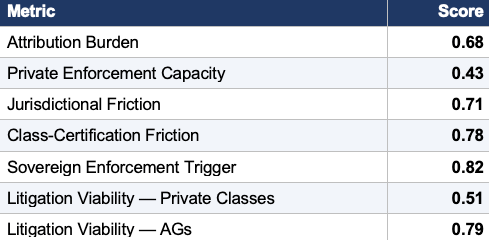

Attribution Cost Vision

Function. Attribution Cost Vision evaluates when private actors cannot efficiently prove responsibility, scope, or remedy and the enforcement pathway migrates toward sovereign actors, measuring attribution burden, enforcement capacity, jurisdictional friction, class-certification friction, and remedy migration pressure.

Reading. Private buyers can identify their own fee, but private classes must prove common policy, disclosure timing, contract language, service basis, and injury across state-specific transactions. AGs face lower aggregation friction — they subpoena before proving commonality, investigate state-specific practices without certifying a class, and proceed under consumer-protection authority even where antitrust damages theories hit indirect-purchaser, standing, or certification barriers. Batton strengthens the AG vector by showing private buyer claims surviving and narrowing at once, leaving a gap AGs can step into.

— Enforcement migrates toward AGs: 75–85% if state copycat suits emerge.

— Private national class certification stays structurally difficult: 65–80% given varying forms, disclosures, agreements, and arbitration provisions.

— State subclasses outperform a national class: 65–80%.

— AG subpoenas target policy attribution before market definition: 70–85%.

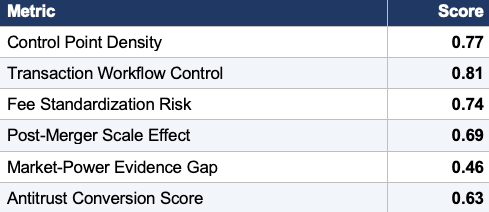

Platform-Control Vision

Function. Platform-Control Vision evaluates whether a firm controls enough transaction chokepoints to convert scale into monetization power, tracking inventory visibility, user routing, workflow control, fee standardization, settlement integration, data visibility, and revenue capture.

Reading. The platform theory gains force when enforcers connect the fee to multiple chokepoints: private listings (visibility), agent routing (buyer access), referral systems (economic routing), transaction software (workflow), title and escrow adjacency (closing leverage), and flat fees (direct monetization). The central distinction: a brokerage can charge a fee, but a platform with scale, data, workflow control, and routing can impose fees consumers struggle to discipline through ordinary choice. Market-power evidence remains the gap — the fee needs local share, agent density, private-listing share, buyer-flow dependence, adoption rates, waiver rates, and avoidability data.

— Platform-control evidence strengthens merger or conduct scrutiny: 55–70%.

— Fee data grows more useful paired with local concentration data: 70–80%.

— Antitrust pleadings on the fee alone stay weak: 60–75%; the fee as one piece of broader platform conduct performs materially better.

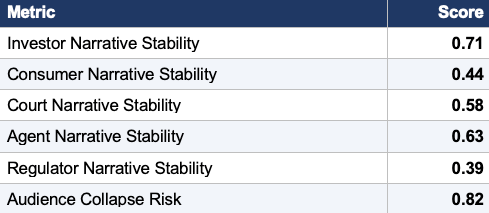

Narrative Integrity Vision

Function. Narrative Integrity Vision evaluates whether a company can maintain coherent explanations across investors, courts, regulators, agents, consumers, and the press, testing narrative consistency, audience separation, contradiction risk, and rebuttal durability.

Compass faces narrative compression: investors hear revenue, consumers hear a routine closing charge, courts hear a signed document, agents hear standard practice, regulators hear platformized extraction. Once plaintiffs place SEC language, contract language, closing-statement language, and agent guidance into one record, Compass loses the ability to keep each explanation separate — the audience collapse the MindCast: Narrative Inversion Playbook and MindCast: Strategic Antitrust Forum Shopping analyses anticipate.

— Compass defends the fee as disclosed and standard: 80–90%.

— Plaintiffs and AGs characterize the fee as platformized extraction: 70–80%.

— Investor-facing disclosures become cross-examination material: 70–80%.

— Narrative pressure intensifies if discovery shows standardized schedules, automated software fields, or closing instructions: 80–90%.

Combined Forecast

Compass’s transaction-fee problem will most likely develop as a consumer-protection and AG-investigation issue first, then become antitrust evidence inside a broader platform-control and merger-scrutiny theory. Combined confidence band: 80–85%. The fee need not prove monopoly power; it needs only to show how Compass monetizes transaction control after buyers enter the funnel. The Florida complaint supplies consumer-payment proof, the SEC disclosure supplies revenue-recognition proof, the platform architecture supplies the control path, and Batton supplies the AG-vector logic.

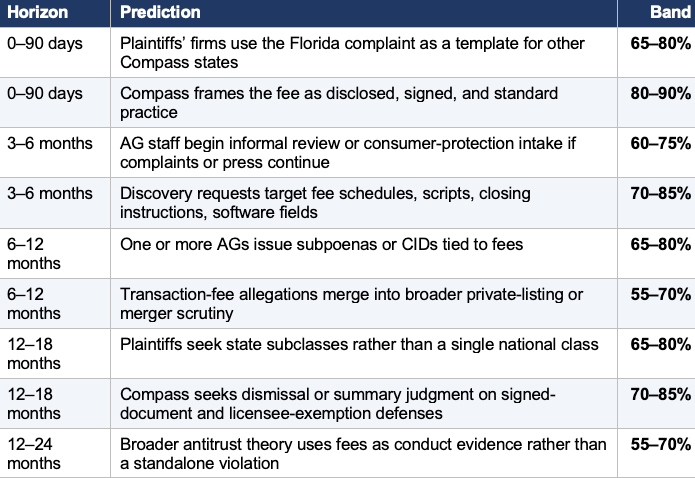

Prediction Table by Time Horizon

Key Metrics for Ongoing Monitoring

Scenario Forecasts

Scenario 1 — Consumer-Protection Expansion (65–80%)

Best evidence: Purchase contracts, closing statements, fee schedules, waiver records, consumer complaints.

Compass defense: Signed documents, clear settlement statement, industry custom, broker-license exemption.

MindCast reading: Consumer-protection claims carry the strongest near-term pathway.

Scenario 2 — State Copycat Class Actions (75–90%)

Best evidence: Similar fee language across transactions and states.

Compass defense: State-law variation, different buyer agreements, different agent disclosures, arbitration provisions.

MindCast reading: State copycats look more likely than one national class.

Scenario 3 — AG Platform-Control Investigation (55–70%)

Best evidence: SEC fee recognition, private-listing data, post-Anywhere integration records, software workflows, market-share concentration.

Compass defense: Fee legality, lack of market power, ordinary brokerage practice, consumer choice.

MindCast reading: Platform-control scrutiny becomes the highest-value antitrust path.

Scenario 4 — Standalone Antitrust Fee Claim (25–40%)

Best evidence: Uniform fee, limited consumer avoidability, local market power.

Compass defense: Unilateral pricing, disclosed fee, no agreement, no exclusionary conduct, no market-power proof.

MindCast reading: The standalone antitrust theory stays weak unless discovery reveals coercive routing, tying, or market-level exclusion.

Scenario 5 — Compass Containment (45–60%)

Best evidence: New buyer-agreement language, fee opt-out policy, refunds, revised closing instructions.

Compass defense: Remediation and clarification.

MindCast reading: Containment reduces consumer-protection risk but may validate the inference that prior disclosures created vulnerability.

Publication Interpretation

The simulation identifies the transaction-fee dispute as an enforcement bridge, not a standalone endpoint: the Florida complaint gives AGs a document set, the SEC disclosure gives them a corporate-policy question, the platform model gives them a control theory, and Batton gives them a reason to view private buyer litigation as incomplete.

Publication claim. Compass’s transaction-fee exposure matters because the fee converts a private-listing transparency dispute into a transaction-platform control inquiry. A $475 charge does not prove antitrust harm; a $475 charge recognized as corporate revenue, inserted into transaction documents, and collected inside an end-to-end brokerage workflow gives attorneys general a concrete way to test whether Compass’s scale lets it monetize control points ordinary competition should constrain.

Regulator-facing claim. Attorneys general should subpoena the fee architecture before debating the antitrust label. Fee schedules, software fields, closing instructions, waiver records, consumer complaints, and revenue accounting will show whether the fee reflects ordinary brokerage practice or platformized extraction.

Public-facing claim. Compass may not merely control when buyers see homes. Compass may also control how buyers encounter transaction costs after they enter the deal.

XII. Related MindCast Corpus

Compass private-listing work identified inventory-visibility control. Compass commission-consolidation work identified internal economic capture. Compass–Anywhere work identified scale expansion. The Florida transaction-fee complaint now supplies consumer-payment proof, and the SEC disclosure supplies corporate revenue recognition. Together, the corpus moves the analysis from a transparency harm to platformized transaction extraction — the same arc this brief traces from visibility control to closing-table monetization.

Foundational

— Why Compass Needs Private Listings — The Inventory-Routing Premium, the Anywhere Merger, and the Multi-State Enforcement Window — the immediate predecessor; fees supply the consumer-harm bridge AGs can use before proving the full private-listing theory.

— Compass’s Interpretation of “Public Marketing” May Draw Antitrust Scrutiny from State Attorneys General — frames the definitional fight over “public marketing” that the fee dispute extends from listing visibility to transaction cost.

— Compass’s Skillman Moment Reaches the C-Suite; the Cris Nelson Moment Holds at the Regional Tier — tracks how local control escalates to the corporate tier — the same scale-of-control logic the fee architecture exposes.

Most directly relevant

— The Compass Commission Consolidation Strategy — commission capture extends from private inventory to standardized closing-table monetization.

— The Compass–Anywhere Address Suppression Calculus (Team Foster) — pairs pre-market visibility suppression with post-contract fee extraction at the transaction level.

— Letter to State Attorneys General on the Compass–Anywhere Merger — the procedural bridge; the fee adds a consumer-payment hook to the existing merger-scrutiny ask.

— Compass’s Strategic Antitrust Forum Shopping — investor-facing revenue disclosure versus litigation-facing minimization of the same fee.

— Amicus Curiae Brief in Support of NWMLS — transparency as market-protective infrastructure, extended from listing visibility to fee visibility.

Strong supporting

— Compass v. NWMLS — The Counterclaim — conduct marketed as innovation becomes evidence of control once adversaries place the documents in the record.

— The Antitrust Litigation Trap Compass Built (Visual Synthesis) — the most damaging record is self-generated: contracts, closing statements, SEC disclosures.

— The Compass Narrative Inversion Playbook — control reframed as choice; exclusivity as empowerment; transaction fees as standard practice.

— The Cybernetics of Compass’s Narrative Control Architecture — the shared fee category collapses audience separation between investor and consumer narratives.

— The Compass-Reffkin Consumer Policy Center (Self-Disclosure Trap) — public records reveal the revenue architecture before regulators need discovery.

— Compass Rhetorically Reframing MLS Transparency — converts a public market-transparency question into a private contract-consent question.

— Compass Plan B: Structural Circumvention After SSB 6091 — tests whether fees rebuild value as transparency statutes close private-listing windows.

— SSB 6091 Has Passed — What It Means for Enforcement — Washington enforcement architecture gains a new evidence class: purchase contracts and closing statements.

Broader framework

— Chicago School Accelerated, Part I: Coase — the $475 fee matters because it exposes who controls transaction architecture, not because $475 proves harm.

— When Antitrust Becomes Theater — the fee enters the infrastructure-litigation record as a material business practice, not an isolated dispute.

— The Prediction Markets Rule Architecture (definitional method) — method for forcing definitional clarity across overlapping fee labels — who sets it, who earns it, when consumers learn of it.

Infrastructure Routing Control (AI energy markets) maps by analogy — inventory, agent, referral, workflow, and closing-fee routing as one control architecture — and should be added once its final slug is confirmed.

XIII. URLs Provided and Referenced

Batton order: Batton v. Compass, Inc., No. 1:23-cv-15618 (N.D. Ill.), Memorandum Opinion and Order (Mar. 24, 2026) (Hunt, J.). Cite the PACER docket entry or court-hosted PDF when placing this reference; the docket-posture facts above (settlements, stays, opt-ins) rest on trade-press reporting and should be confirmed against the filings before distribution.

Uploaded complaint file: Compass Commission Lawsuit FL.pdf

Real Estate News article provided by user: https://www.realestatenews.com/2026/06/26/compass-transaction-fees-under-fire-in-new-class-action-suit

Complaint PDF previously referenced: https://assets.ctfassets.net/hzfwsdcegxo2/4F7Igxuc8slh46hW6cJ5xW/b10c7036251acb2b91ff195f84a7807f/EfronvCompassFlorida_Complaint_06232026.pdf

Florida Deceptive and Unfair Trade Practices Act reference: https://www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&URL=0500-0599/0501/Sections/0501.204.html

Florida Consumer Collection Practices Act reference: https://www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&URL=0500-0599/0559/Sections/0559.72.html

Florida Bar consumer real estate guidance reference: https://www.floridabar.org/public/consumer/pamphlet006/

The Real Deal article on Compass transaction fees and referral program: https://therealdeal.com/national/2026/02/26/compass-unveils-lead-referral-program-transaction-fees/

NAR written buyer agreements reference: https://www.nar.realtor/the-facts/written-buyer-agreements-101

NAR consumer guide to written buyer agreements: https://www.nar.realtor/the-facts/consumer-guide-to-written-buyer-agreements

Compass Q1 2026 investor results reference: https://investors.compass.com/news/news-details/2026/Compass-Inc--Reports-First-Quarter-2026-Results/default.aspx

Compass SEC filing reference: https://www.sec.gov/Archives/edgar/data/1563190/000156319026000057/comp-20251231.htm

Wall Street Journal report on New York AG scrutiny of Compass: https://www.wsj.com/real-estate/real-estate-giant-compass-under-antitrust-investigation-in-new-york-29bd0e74

Appendix A. Confidence Band Register (Methodology)

Each band below expresses directional confidence in an inference drawn from the record, not a probability of any litigation outcome. The register fixes every inferential proposition to a single band so that no claim carries two numbers across sections. Two distinctions hold the table together. Doctrinal viability — whether a theory is legally cognizable — is tracked separately from procedural survival of a specific vehicle, which is why the transaction-fee theory sits at ≈75% while the Florida FDUTPA vehicle that carries it sits at ≈65%, depressed by the licensee-exemption fact contest. Band movements observe one-increment discipline: only two AG bands moved from prior estimates, each by a single step.

Anchors reference the section where each proposition is introduced and where it is developed. Batton throughout denotes persuasive parallel reasoning rather than controlling authority, usable by either side and read here as net favorable to plaintiffs on the documentary-record distinction.