MCAI Lex Vision: Why Compass Needs Private Listings, The Inventory-Routing Premium — Compass, the Anywhere Merger, and the Multi-State Enforcement Window

How a Documented Multi-State Pattern of Listing-Control Conduct Frames the Antitrust and Consumer-Protection Questions Now Before State Enforcers — With New York as the Live Test Case

Executive Summary

Compass, Inc. completed its acquisition of Anywhere Real Estate on January 9, 2026, after significant congressional scrutiny concerning listing transparency, private listing networks, and residential real-estate competition. Since the merger closed, Compass has participated in a coordinated campaign involving multiple regional listing services, identity-protective listing rules, and private-listing infrastructure designed to reshape how residential inventory reaches consumers. New York’s investigation arises within that broader national pattern, and attorneys general in eleven other states whose congressional delegations questioned the deal hold the same jurisdiction to examine it.

A single theory explains why Compass devotes so much effort to listing rules: the merger economics depend, in part, on preserving inventory-routing advantages that disappear when concurrent-marketing laws eliminate the private phase.

Part of Compass’s acquisition value rests on the ability to withhold a listing from the open market long enough for an internal buyer to arrive first, capturing both sides of the commission. State transparency statutes extinguish that advantage locally. The coordinated listing-service campaign rebuilds it externally, in jurisdictions that have not yet legislated. A company that went public in 2021 as “a real estate technology company” is now defending its valuation through debt-backed consolidation and listing-rule manipulation rather than through any product — and a genuine technology advantage would not vanish when a state mandates concurrent marketing. An investigator need not endorse this theory to find it the most economical explanation of the conduct — and the question it raises is precisely the one a state enforcer is positioned to answer.

Washington supplied the first statutory test of the private-listing model. Illinois supplied the first coordination allegations in federal court. New York now holds the first large post-merger opportunity to evaluate whether the pattern produces measurable consumer harm. The pages that follow document the conduct, trace the pattern across those three states, state a theory of harm, and identify specific, narrow questions a state review can resolve without proving a nationwide conspiracy.

I. Why This Memorandum, and Why Now

Compass completed the largest brokerage combination in the country’s history and then, within weeks, moved to secure identity-protective rules at four regional listing services while terminating its direct listing feeds to the dominant consumer portal. The conduct is documented, recent, and concentrated in the months following the merger’s close. New York opened its review against that backdrop.

The conduct described below forms a coherent and testable pattern across multiple jurisdictions. The events are not a chronology of unrelated commercial decisions; they trace a single strategy operating wherever local law has not yet foreclosed it. The pages below document that pattern, state a theory of why the conduct occurs, and identify the narrow questions a state review can resolve.

Federal review and state review answer different questions. Federal merger review evaluates a transaction prospectively — whether a deal should close. State attorneys general evaluate market conduct retrospectively — what a firm does after it closes. The question before New York is therefore not whether the Compass–Anywhere merger should have been approved in January 2026. The question is whether post-merger conduct has produced competitive effects, consumer harm, or deceptive practices within New York’s jurisdiction. The federal process closed without resolving it, and it sits squarely within state authority.

The analysis speaks to several audiences at once. For state attorneys general, it maps how the Washington and Illinois records transfer to other jurisdictions and identifies the enforcement surface each state’s law already provides. For members of Congress who have questioned the merger, it connects the federal review record to the state-level remedies that remain available. For multiple-listing-service and listing-service leadership, it identifies the specific governance decisions that determine whether a regional cooperative becomes a vector for the pattern or a firebreak against it.

II. The Congressional Record Already Names This Deal

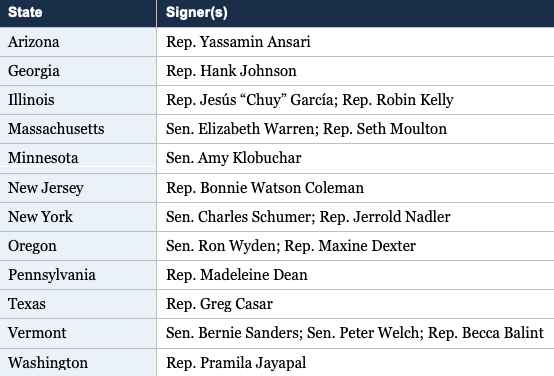

Two letters to federal authorities establish that the merger drew sustained congressional scrutiny before any state acted. In December 2025, Senators Elizabeth Warren and Ron Wyden urged the Department of Justice and Federal Trade Commission to investigate the transaction, citing transparency, broker fees, and private-listing-network concerns. In February 2026, Representative Becca Balint and Senator Warren led a second letter to the Attorney General, signed by nineteen members of Congress, questioning the circumstances under which the DOJ cleared the deal and posing seventeen detailed questions about the review.

The signers represent twelve states. An attorney general in any of these states can point to a sitting member of that state’s own congressional delegation who has already flagged the merger — converting a federal political signal into local support for state enforcement action.

Illinois, Washington, and New York now occupy the center of the litigation and regulatory record. Illinois is the venue of the federal coordination case; Washington is the home of the first transparency statute; New York hosts both the new attorney-general review and the recently passed listing-transparency act. The federal signal and the state record reinforce each other most directly in exactly those jurisdictions.

III. The Documented Pattern, Stated Plainly

Compass executed a coordinated multiple-listing-service rule-capture campaign across at least four major regional services between October 2025 and May 2026. Midwest Real Estate Data in Chicago, Realtracs in Nashville, The MLS/CLAW in Los Angeles, and Bright MLS across the Mid-Atlantic each adopted identity-protective listing rules and opened nationwide membership under partnership terms with Compass International Holdings. Each service adopted the same rule template, named Compass as a launch partner, and accepted Compass subsidies for agents who joined.

CEO Robert Reffkin committed to the strategy on the record during the May 5, 2026 earnings call, stating that he wanted to create a national listing service to compete against local ones. Seven days later, Zillow filed a federal antitrust complaint in the Northern District of Illinois alleging the partnerships operate as a coordinated Sherman Act conspiracy designed to coerce portal compliance under threat of feed termination. MindCast analyzed how the filing reframes the dispute as a national coordination case in How the Zillow Complaint Reframes Compass v. NWMLS as a National Coordination Case.

An irony sits at the center of the conduct. Compass went public in April 2021 branded as “a real estate technology company,” priced for the valuation Wall Street reserves for an extraordinary technology product, with its S-1 forecasting that it might pursue larger acquisitions to add technology and adjacent services. Five years later, the company is pursuing debt-backed acquisitions to consolidate agent count and market share, and defending that position by reshaping listing rules rather than by shipping a product. The tell is structural: a genuine technology advantage does not evaporate when a state passes a concurrent-marketing statute. A state listing law can nonetheless threaten a material share of the merger’s value — the MindCast three-layer model estimates the private-inventory premium at $400 to $800 million (The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency), and a value that a marketing statute can erase was never located in technology or business-model innovation — it lay in the ability to control which buyers see which listings, and when. The post-merger campaign is consolidation and inventory control, not invention. Appendix B sets out the estimate’s inputs, method, and sensitivity range.

The economic engine carries a name worth retaining: forced reconstruction of withheld-inventory value. Compass’s acquisition premium depends on a layer of value that exists only when listings can be withheld from the open market long enough for an internal buyer to capture both sides of the commission. State transparency statutes extinguish that layer locally. The rule-capture campaign rebuilds it externally, in jurisdictions that have not yet legislated. The campaign becomes economically understandable as a response to a closing legal window rather than as opportunistic expansion. MindCast develops the three-layer acquisition model in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency and applies it to the litigation record in Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis.

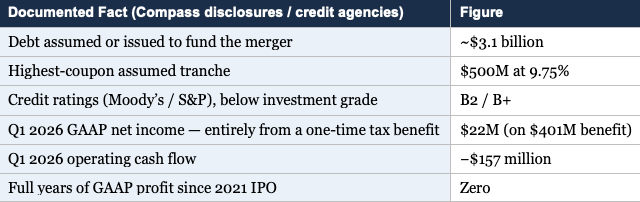

The Financial Spine — Why the Engine Has to Run

The economic logic is testable against Compass’s own disclosures, and an investigator can verify each figure below from public filings. To fund the Anywhere transaction and refinance Anywhere’s capital structure, Compass assumed or issued roughly $3.1 billion in long-term debt, including senior secured and unsecured notes and $1.0 billion of 0.25% Convertible Senior Notes due 2031; total long-term debt stood at $3.14 billion at March 31, 2026. Among the assumed notes is a $500 million tranche carrying a 9.75% coupon. Moody’s and S&P rated the post-merger entity at B2 and B+ — below investment grade. The company’s Q1 2026 GAAP net income of $22 million was produced by a one-time $401 million non-cash deferred-tax benefit; without it, the quarter was a loss, and operating cash flow was negative $157 million. Compass has not reported a full year of GAAP profitability since its 2021 IPO.

Those facts connect directly to the conduct. A firm servicing $3.1 billion in below-investment-grade debt, including a tranche at a 9.75% coupon, with no history of full-year GAAP profit and a quarter that turned positive only on a non-cash tax item, needs durable operating margin. The private-listing architecture is where Compass’s own investor and marketing communications locate that margin: by routing a listing through the Compass network and placing a Compass-represented buyer, the firm captures both the listing-side and buyer-side commission on a single transaction. State concurrent-marketing statutes remove the withholding window that makes the double-sided capture reliable. The multi-state listing-service campaign began immediately after the merger closed and operates precisely in the jurisdictions where those statutes do not yet exist. An investigator does not have to accept that sequence as intent; the public financials, the credit ratings, the earnings-call commitments, and the timing of the campaign are each independently verifiable, and together they let a reviewer evaluate the theory rather than reconstruct it.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

IV. The Washington Record — The Pattern’s First Statutory Test

Washington enacted SSB 6091 in March 2026, effective June 11, 2026, prohibiting the off-market closed-loop model unless a property is marketed publicly on a concurrent basis. The statute and Compass’s response to it produced the clearest record of how the pattern behaves under legal pressure. Two named diagnostics emerged from the Washington record and now travel to other states.

The Skillman Moment. Compass’s seller-choice narrative coheres inside its own commercial environment but fails the instant it contacts a statutory or evidentiary record outside that environment. A Compass broker applied the firm’s listing-service framing to a state licensing statute on the day the governor signed it; the framing collapsed because the two legal regimes do not match. The same category error then reappeared, verbatim at the framework level, in the CEO’s earnings-call statements seven weeks later. MindCast formalized the mechanism in The Cybernetics of Compass Holdings’ Narrative Control Architecture and traced its boundary condition in The Skillman Moment as Analytical Rosetta Stone.

The Cris Nelson Moment. Accountability breaks down at the regional-executive tier through structural silence. Compass’s Pacific Northwest Regional Vice President attended both Washington legislative hearings, declined to testify, and issued no attributed post-passage statement — even as front-line brokers absorbed the public exposure. The silence is itself the specimen: it marks the layer where the campaign’s jurisdiction-dependent legal architecture could not be articulated without exposing it. Compass’s Skillman Moment Reaches the C-Suite, Cris Nelson Moment Holds at the Regional Tier documents the pattern reaching the C-suite while the regional tier holds silent.

The Testimony Record — What Compass Said, and Declined to Say, Under Oath

Washington’s legislative record holds testimony of direct use to a state enforcer, because legislative testimony enters an official public record and carries evidentiary weight that trade-press statements do not. The Senate Bill Report lists Brandi Huff, Compass’s Managing Director for Washington, among the witnesses who testified in opposition to SSB 6091 at the January 23, 2026 Senate Housing Committee hearing. Her exchange with the committee is the record’s most consequential moment.

Senator Emily Alvarado asked how Compass’s position as the largest Wall Street-backed brokerage in the country interacts with exclusive networks. Huff confirmed the model functions “specifically with the amendments.” When Chair Jessica Bateman pressed — “But without the amendments?” — Huff answered: “That is probably above what I feel comfortable speaking to.” A senior Compass executive, on the record and on exactly the question a state attorney general is now asking, declined to address how the model functions without the amendments. The exchange places the merger and the exclusive-network model in direct contact on the legislative record and leaves the question unresolved by the company representative, in a forum that produces admissible evidence.

The two tiers form a single specimen. Huff testified and reached the limit of what she would say about the merger’s relationship to the inventory model; Nelson, the more senior regional executive, attended the same hearings and declined to testify at all. One executive’s candor stopped at the decisive question and the other’s participation stopped before it — a paired pattern more telling than either silence alone. Compass also told the House committee that public data access amounts to predatory “scraping,” a characterization that supplies a procompetitive justification for the very transparency rules Compass challenges in its own federal litigation. The Washington testimony record therefore gives a state reviewer an admissible near-admission on the merger question and a legislative argument that cuts against Compass’s federal posture.

The Astroturf Coefficient — Manufactured Opposition Measured Against Its Own Result

Beneath the executive testimony sat a coordinated grassroots-opposition apparatus that the legislative record allows an enforcer to quantify. At the January 23, 2026 Senate hearing, 162 individuals affiliated with Compass registered opposition to SSB 6091; only nine disclosed that affiliation — a ratio of roughly seventeen undisclosed Compass affiliates for every one who disclosed. Regional Vice President Cris Nelson was among those who signed in opposed without disclosing the Compass relationship. Between the Senate hearing and the January 28 House hearing, Compass-affiliated sign-ins fell sixty-seven percent, from 162 to 54, as the disclosure pattern became visible. The Compass Astroturf Coefficient at the Washington State Senate.

Supporting infrastructure carried the same design. VoterVoice campaigns supplied pre-drafted opposition messaging and collected agents’ mobile numbers for coordinated activation, and a consumer-facing site, compass-homeowners.com, advanced a 2.9 percent price-premium claim that compares Compass listings only to other Compass listings rather than to the open market. The apparatus’s actual persuasive yield is the tell. SSB 6091 passed 141 to 1 across both chambers — 49–0 in the Senate, 92–1 in the House. A large, coordinated, substantially undisclosed opposition operation moved exactly one vote in a closely divided legislature. MindCast formalized the disclosure asymmetry as the Astroturf Coefficient and documented it in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency. For a state reviewer, the metric matters twice: it is a measurable indicator of manufactured rather than organic opposition, and the undisclosed-affiliation pattern is itself potentially actionable conduct.

The contradiction is not between what Compass tells courts and what it tells legislatures. Those two stories align: in both forums Compass advances a consistent “seller choice” narrative, defending private listings as a consumer option. The divergence sits one layer down — between that public-facing choice narrative and what Compass tells shareholders and its own agents. To investors, private listings are not a consumer accommodation; they are the business model. They are how a firm carrying billions in acquisition debt and no history of full-year GAAP profit generates margin: by holding inventory inside the Compass network long enough to place a Compass buyer, capturing the commission on both sides of the same transaction. Compass’s Cross-Forum Contradictions.

Read against the investor record, the “choice” vocabulary inverts in meaning. The objective is not to widen the seller’s options; it is to narrow the buyer’s. Every listing held off the open market is a buyer who must come to Compass to see it — and, increasingly, a buyer a Compass agent then represents. The mechanism boxes consumers into the Compass funnel so that Compass can harvest the double-sided commission, and the seller-choice language is the public name for a buyer-restriction architecture. MindCast traces how the narrative is constructed and deployed across audiences in The Compass Narrative Inversion Playbook. The investigative question for a state enforcer is therefore not whether Compass said inconsistent things to two courts; it is whether the conduct Compass markets to investors as a profit engine produces, for consumers, the reduction in competition and access that the public narrative is designed to obscure.

The forecast has already partially resolved true ahead of schedule. Connecticut Governor Lamont signed a concurrent-marketing law on May 27, 2026; Wisconsin enacted one in December 2025; New York has now passed its own; and Illinois and Hawaii have bills pending. The prediction record is auditable today, not at some distant horizon.

V. The Legislative Wave — New York as the Newest and Sharpest Instance

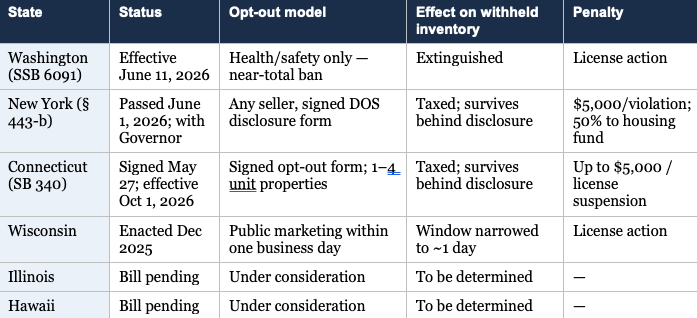

Six states have now moved against private listing networks within roughly six months, and the cluster is what makes the conduct a multi-state enforcement question rather than a local one. Washington’s SSB 6091 takes effect June 11, 2026. Wisconsin enacted a public-marketing requirement in December 2025. Connecticut’s SB 340, signed May 27, 2026, takes effect October 1. Illinois and Hawaii have bills pending. New York passed its own statute on June 1, 2026, and it is the newest and, for enforcement purposes, the sharpest — which is why it serves here as the worked example of how the pattern meets a state law.

New York’s Fair and Transparent Real Estate Listings Act cleared both chambers. The Assembly vehicle, A10679-B, sponsored by Assemblymember Solages, was substituted for and passed in place of Senate Bill S10274, sponsored by Senator Fernandez, on June 1, 2026. The Senate vote was 60–0. The bill has been delivered to Governor Hochul; the enacted text takes effect on the 180th day after it becomes law. Reviewers should confirm signing status before relying on an effective date.

The operative mechanism is a dedicated concurrent-marketing duty. New Real Property Law § 443-b, subdivision 2(E), requires a listing agent to concurrently and publicly advertise any property listed on private or limited-access channels. The provision targets private listing networks by name and defeats the sequencing that the multi-phase marketing strategy depends on. Industry coverage captured the point precisely: the word “concurrently” erases the head start, because there is no quiet phase if the public phase must happen on day one. The duty is the common spine across all six statutes; the states differ mainly in how a seller may opt out of it.

New York’s opt-out architecture is what makes it the sharpest enforcement instrument. Washington extinguishes the withheld-inventory layer almost entirely, allowing exceptions only for health or safety. New York and Connecticut instead permit the seller to opt out by signing a standardized state disclosure form that spells out the risks — reduced visibility, fewer offers, and possible impact on price and timing. The disclosure route taxes the withheld-inventory layer rather than eliminating it: the private phase survives behind a signed form — and every signed form is a record.

The disclosure model is an enforcement advantage, not a weakness. Because New York routes the conduct through a mandatory written disclosure, every withheld listing generates a retained, three-year, subpoenable record. The statute also forecloses the predictable narrative response: subdivision 5(C) bars an agent from altering or softening the disclosure language. Section 4 raises the licensing fine ceiling from $2,000 to $5,000 per violation and directs half of all such fines to the state’s anti-discrimination in housing fund — tying enforcement directly to the fair-housing findings that open the Act. Connecticut’s SB 340 carries a comparable signed-opt-out structure and penalties up to $5,000, so the same record-generating logic applies in any disclosure-model state.

VI. The Six-State Statutory Map

The statutes share one duty — concurrent public marketing — and diverge on the opt-out and the penalty. The map below lets an enforcer in any of these states see at a glance which model its own law follows, and therefore which enforcement record the conduct will generate locally.

Two enforcement models emerge. The Washington model bars the conduct outright and produces little evidentiary record because the conduct simply stops. The disclosure model — New York and Connecticut — permits the conduct behind a signed form and therefore generates a per-listing, retained, subpoenable dataset. A state in the disclosure column has the stronger investigative record; a state in the ban column has the cleaner prohibition. Illinois is also the venue of the federal coordination case, which gives an Illinois enforcer a second, litigation-based record independent of whatever statute it ultimately passes.

VII. How the Theory Transfers to Any State

The enforcement theory does not depend on a single state’s statute; it depends on three elements that recur in every market where Compass operates, and an enforcer in any state can test for each. The first is market power — whether the merged entity concentrates agents, brands, and listing-service relationships in the local market. The second is a routing incentive — whether the firm has reason and means to keep inventory inside its own network. The third is consumer harm — whether the practice measurably reduces competition, visibility, or choice against an open-market baseline. The legal vehicle then varies by state: a federal Sherman Act theory where a captured-rule event has occurred, or state antitrust and consumer-protection law where it has not.

New York is the worked instance. The federal Sherman Act group-boycott theory from the Illinois litigation does not port cleanly to New York, for two reasons: the REBNY Residential Listing Service is not technically a multiple listing service, and no captured-rule event has yet occurred in the New York market. A New York theory rests instead on state law — the Donnelly Act for any coordination that emerges, and General Business Law § 349 for deceptive practices, anchored to the § 443-b public-policy standard. Every state has the analogous pair: a state antitrust statute and a consumer-protection or deceptive-practices act. The New York mapping shows how to select the vehicle; the selection repeats in each jurisdiction.

The market-power element is already present in the largest markets. The Anywhere merger consolidated Corcoran and Sotheby’s International Realty — core New York City luxury brands — under the same holding company running the national campaign, and the same brands (Coldwell Banker, Century 21, Sotheby’s, Corcoran, ERA, Better Homes and Gardens) concentrate share in major markets nationwide. The consumer-harm element is supplied by Compass’s own materials and is jurisdiction-independent: in the Washington litigation, the Northwest service, drawing on Compass marketing data, asserted that listings fail to sell during the private phases roughly 95 percent of the time before reaching the open market. A figure drawn from Compass’s own data, not from any one state’s record, attacks the consumer-benefit premise in every state at once. MindCast traced the address-suppression mechanics in The Compass-Anywhere Address Suppression Calculus — Team Foster Scenario.

A market signal points enforcers toward the participants who can document the conduct. In New York, Brown Harris Stevens publicly supported the transparency legislation and mobilized its agents in favor, while the statewide Realtors association stayed neutral and hedged in seller-choice language. A direct luxury competitor whipping votes for transparency marks where inventory-control advantage concentrates — and identifies a market participant with both knowledge of the conduct and an incentive to document it. The same tell is available in any state: the competitor who breaks ranks to support the statute is the competitor who has felt the routing advantage operate against it.

VIII. Three Monitoring Targets for Enforcement

The conduct pattern points to three places a state review can look first, each chosen because the evidence already exists in a form an enforcer can compel or observe. In a disclosure-model state, the statute itself creates the first two records; the third sits in listing-service governance everywhere. Taken together, the three targets convert the broad theory of harm into specific, checkable conduct, and each is described in the New York terms where the statute is furthest along — with the state-law hook named so an enforcer can substitute the local equivalent.

1. Opt-out as default rather than exception. Investigators should test whether Compass-affiliated brokerages route sellers to the opt-out form as a standard practice rather than a genuine, informed exception — under New York’s § 443-b, Connecticut’s SB 340, or any disclosure-model statute. The retained forms are the dataset; a systematically high opt-out rate within one brokerage is the signal.

2. Softened or reframed disclosures. New York’s subdivision 5(C) bars altering the mandatory language, and parallel anti-circumvention provisions appear in the other disclosure-model statutes. Any disclosure that recasts the stated risks in seller-choice framing is both a statutory violation and a documented instance of the narrative pattern traced throughout these records.

3. Listing-service governance. Listing-service leadership in any market should watch for a rule change — particularly one propagating through shared technology vendors — that introduces identity-protective feed language or conflicts with the concurrent-marketing default. New York’s REBNY RLS is the local instance; the shared-vendor channel was the propagation vector in the Illinois record, and the same vendors serve services nationwide.

Each target produces a discrete, documentable finding rather than a judgment about Compass’s intent. An enforcer can resolve all three from records the statute requires brokerages to keep, the disclosures they actually deliver, and the rule changes a listing service publishes — without waiting for discovery or litigation to begin.

IX. A Direct Word to Listing-Service Leadership

Multiple listing services and regional listing cooperatives are not bystanders to the pattern described here; they are the infrastructure the pattern operates through. A brokerage cannot withhold inventory from the open market, or compel a portal to display protected listings, without rules that permit it. The rule-setter is therefore the decision-maker, and the decisions are being made now, listing service by listing service, in real time across the country.

Two paths diverge at that decision. A service that adopts identity-protective rules and names a single brokerage as a subsidized launch partner converts itself from a neutral cooperative into a controlled distribution channel — and, as the Illinois complaint demonstrates, into a named defendant’s co-conspirator allegation. The four services already partnered with Compass sit on that path. A service that holds the concurrent-marketing default and keeps its rules brokerage-neutral takes the other: it remains a cooperative utility, and it becomes a firebreak against the campaign rather than a conduit for it.

The distinction matters most for services that have not yet been approached. The Illinois record shows the template arriving through shared technology vendors before it arrives through a formal partnership announcement, which means a board can find its rules altered before it has consciously chosen a side.

Listing-service leadership protects its members and its own legal exposure by treating any identity-protective rule proposal, from any source, as a governance decision that belongs to the board — not a technical update that passes through a vendor. The choice is governance, and the record of how each service makes it is now part of the public file.

X. The State Investigative Mandate

New York does not need to prove a nationwide conspiracy to justify investigation. A state review can resolve three narrower questions, each answerable from records a state enforcer can compel:

1. Control. Did the Anywhere merger increase Compass’s ability to control listing visibility — through agent count, brand concentration, and listing-service relationships in the relevant market?

2. Routing. Do Compass-affiliated brokerages disproportionately route sellers into private-network or opt-out pathways, relative to open-market distribution and relative to competing brokerages?

3. Harm. Do those practices reduce competition, listing visibility, or consumer choice — and can the reduction be measured against the open-market baseline?

Each state arrives at these questions from a different starting point. Washington supplied the first statutory test; Illinois supplied the first coordination allegations in federal court; Connecticut and Wisconsin added concurrent-marketing duties; New York passed the newest and sharpest disclosure statute. The three questions are the same in every one of them. New York is simply the first large post-merger market where a disclosure statute makes the second question — routing — answerable from a concrete, retained, subpoenable record. An enforcer in any disclosure-model state inherits the same instrument; an enforcer in a ban-model state answers the same questions from market-share and conduct evidence instead. The pattern is national; the first complete test of it is the one a state chooses to run.

APPENDIX A

Recommended Reading and Forecast Record

The analytical record below documents each forecast, its date, and its resolution, and every analysis is traceable to its evidentiary basis across three degrees of cited sources. The entries are grouped by the investigative question each one answers. MindCast welcomes direct engagement with any attorney general’s office, legislative staff, or listing-service board evaluating the pattern described here.

Start Here — The Most Recent Synthesis

Compass’s Skillman Moment Reaches the C-Suite, Cris Nelson Moment Holds at the Regional Tier

The current state of the analysis, tying the nationwide rule-capture campaign to the CEO earnings-call record and the regional-executive silence. It is the single best entry point for a reviewer new to the corpus, because it carries the falsification conditions and the multi-state forecast in one place.

The Economic Engine — Why Compass Cannot Let the Private Phase Die

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency

Develops the three-layer acquisition model that explains the merger price — in particular the withheld-inventory layer that exists only when listings can be held off the open market long enough to capture both commission sides. The model is the foundation for understanding why state transparency laws threaten Compass at the balance-sheet level.

Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis

Shows Compass conceding, in its own filing, that the private phases of its marketing strategy will violate Washington law once the statute takes effect. The concession is the cleanest evidence that the withheld-inventory value is legally fragile, and it transfers directly to any state weighing a similar statute.

The Compass-Anywhere Address Suppression Calculus — Team Foster Scenario

Traces how address and listing suppression operate at the transaction level in the Pacific Northwest, the mechanics behind the abstract “selective visibility” thesis. Useful to an AG building a consumer-harm record, because it works from concrete listing conduct rather than corporate framing.

The Federal Coordination Case — The Sherman Act Theory and Its Limits

How the Zillow Complaint Reframes Compass v. NWMLS as a National Coordination Case

Analyzes the May 2026 federal complaint that recast the Compass dispute as a coordinated multi-MLS conspiracy rather than a regional contract fight. It explains the group-boycott theory a reviewer would adapt — and why the theory needs modification where the local listing service is not technically an MLS.

The Compass / NWMLS Antitrust Landscape

The umbrella analysis of the litigation complex, mapping the federal antitrust, state consumer-protection, and securities-disclosure forums that now surface evidence into one another. It orients a reviewer to which forum carries which evidentiary advantage.

MCAI Lex Vision Visual Synthesis — The Antitrust Litigation Trap Compass Built for Itself

A visual walkthrough of how Compass’s litigation arguments expose it to its own evidentiary record — including legislative positions, such as the data-access “scraping” claim, that undercut its federal theory. It is the fastest way for a time-constrained reviewer to grasp the self-inflicted structure.

The Narrative-Failure Diagnostics — How the Public Story Breaks

The Cybernetics of Compass Holdings’ Narrative Control Architecture

Formalizes the two diagnostics this analysis relies on — the Skillman Moment and the Cris Nelson Moment — and the debt-narrative correlation linking rhetorical intensity to balance-sheet pressure. It is the theoretical core for reading any future Compass public statement against its operational conduct.

The Skillman Moment as Analytical Rosetta Stone

Establishes the boundary condition at which individual narrative failures become systemic exhaustion, and the measurable interval between a corporate framing and its contradiction in the public record. It gives enforcers a repeatable test rather than a one-time observation.

The Compass Collapse — A Post Washington SSB 6091 Passage Reckoning

The post-passage reckoning that scored the Washington forecast against the outcome. It is the proof point that the corpus predicts rather than merely describes, which is what makes the multi-state forecast credible.

The Compass Narrative Inversion Playbook

Documents how the seller-choice narrative is built and deployed across audiences — consistent before courts and legislatures, but inverted against the profit logic Compass presents to investors, where the same private-listing model is the double-sided-commission engine. It supplies the public-narrative-versus-investor-narrative gap a state enforcer can test.

Compass’s Cross-Forum Contradictions

Maps the mutually exclusive positions Compass takes across federal court, state legislatures, investor communications, and consumer marketing, showing how the four-forum record becomes exploitable evidence. It is the companion that catalogs each contradiction an enforcer can place side by side.

The Coordination-vs-Competition Test — Is the Conduct Unlawful or Merely Aggressive?

The Dual Nash-Stigler Equilibrium Architecture

Supplies the formal distinction between capture-enabled defection and ordinary unilateral competition — the precise line an enforcer must draw to characterize Compass’s conduct as coordination rather than hard competition. It is the framework to reach for when the defense argues the behavior is just a firm pursuing its own interest.

The Stigler Equilibrium — Regulatory Capture and the Structure of Free Markets

Diagnoses the conditions under which shared institutional infrastructure becomes captured by a dominant participant and begins operating against its stated purpose. It maps directly onto a listing cooperative adopting identity-protective rules that serve one subsidized brokerage.

Chicago School Accelerated — The Integrated Framework

Integrates Coase on coordination costs, Becker on incentive exploitation, and Posner on institutional learning failure into a single system. The Posner prong grounds the argument that the market cannot self-correct here — that the pattern persists because the institutions meant to check it have stalled.

Chicago School Accelerated, Part III — Posner and Efficient Liability Allocation

Develops the institutional-learning-failure prong in full, explaining why accumulating evidence does not produce self-correction in a captured market. It is the analytical basis for concluding that external enforcement, rather than market discipline, is the operative remedy.

The Regulatory-Comment Record — Positions Already Filed

Comment of MindCast AI on DOJ/FTC Updated Merger Guidance (Docket ATR-2026-0001)

A formal regulatory submission applying these frameworks to current federal merger-review standards. As a filed comment rather than commentary, it carries the procedural weight an enforcement audience expects and situates the Compass analysis within the active guidance debate.

The Equilibrium and Predictive-Infrastructure Framework — The Market-Structure Foundation

The MindCast MLS Equilibrium Series (Umbrella)

The unifying framework treating residential real estate as a captured-equilibrium market, connecting the litigation, the statutes, and the capital-markets implications. It supplies the economic vocabulary an expert report would build on.

Part I — The Equilibrium Selection Problem in Residential Real Estate

Applies the Nash-Stigler architecture to the three available market equilibria and the three forms of defection, grounding the abstract framework in the residential-real-estate facts. It is the bridge between the formal theory and the Compass record.

Runtime Geometry — A Framework for Predictive Institutional Economics

Sets out the predictive method underlying MindCast’s falsifiable forecasts, the machinery that let the corpus call the Washington outcome in advance. Relevant to a reviewer weighing how much forecasting weight to give the multi-state projection.

Constraint Geometry and Institutional Field Dynamics

Formalizes how legal and regulatory constraints reshape institutional behavior over time — the structural account of why each new state statute compresses the room the pattern has to operate. It frames the multi-state legislative wave as a tightening constraint field rather than a series of isolated events.

APPENDIX B

The Private-Inventory Premium Estimate

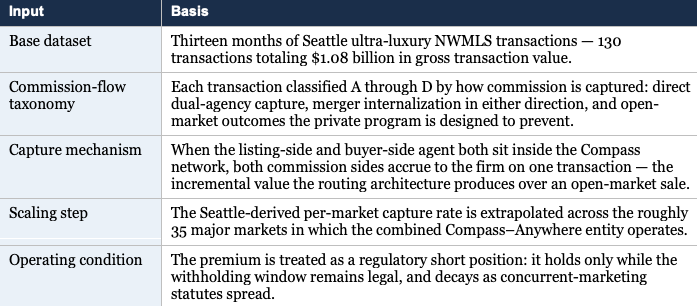

The $400 to $800 million figure cited in the body is a MindCast model estimate, not a Compass disclosure. The estimate is set out below so a reviewer can test the assumptions rather than accept the number. The derivation appears in full in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency; the summary here states the inputs, the method, the scaling step, and the sensitivity range.

What the Estimate Measures

The estimate isolates one component of the $1.6 billion Anywhere acquisition price: the value attributable specifically to operating the private-inventory routing architecture — the “Layer 3” premium. The figure does not measure the whole acquisition. It measures the portion that exists only while listings can be withheld from the open market long enough for a Compass-affiliated buyer to be matched first, allowing Compass to capture commission on both sides of the same transaction. A reviewer should read it as the value at risk when a concurrent-marketing statute removes the withholding window, not as a valuation of the brokerage.

Inputs and Method

Range and Sensitivity

The $400 million to $800 million range reflects the two variables that move the estimate most: the share of network listings that convert to a double-ended, in-network sale, and the degree to which the Seattle ultra-luxury capture rate holds in lower-price and lower-density markets. The low end assumes a conservative conversion rate and meaningful decay when the Seattle rate is applied nationally; the high end assumes the Seattle pattern scales with limited decay. MindCast characterizes the range as conservative, because it is anchored to ultra-luxury data and does not assume the highest observed capture rates extend across the full portfolio.

Verification path. Three of the inputs are independently checkable against public data: the combined entity’s market count and gross transaction value appear in Compass’s Q1 2026 disclosures; prevailing commission rates are a matter of public record; and the spread of concurrent-marketing statutes — which sets the decay rate — is documented in the body of this analysis. The one input proprietary to MindCast is the Seattle transaction-level classification, available in the source publication. A reviewer who substitutes different conversion or decay assumptions can recompute the range; the model’s structure, not the specific endpoints, is the analytical contribution.