MCAI Innovation Vision: New York's Data Center Moratorium — How States, Cities, and Counties Now Regulate New AI Data Center Development — and Why Markets Must Reprice AI as Infrastructure

AI Repricing Series: Permitting Pauses, Grid Funds, Large-Load Tariffs, and the FERC Intervention — Fourteen Falsifiable Predictions and a Model State Framework

AI Repricing Series. AI Repricing Cycle 2026, Microsoft, Oracle, Amazon and the Escape from the AI Repricing Cycle

Companion frameworks: Agent Governance Equilibrium, Chicago School Accelerated, The Dual Nash-Stigler Equilibrium Architecture, the AI Accountability series, Agentic Duty of Care, and Foresight Before Disclosure

Executive Summary

Markets still value much of artificial intelligence through software economics. Governments have started regulating the physical production of AI as infrastructure. On July 14, 2026, that gap became law: New York Governor Kathy Hochul signed Executive Order 62 (EO 62), the first statewide moratorium on large data centers in the United States, pausing environmental permits for any facility drawing 50 megawatts or more while the state writes rules for the industry. Nearly 12 gigawatts of data center demand — roughly the output of twelve nuclear reactors — now waits in New York’s grid queue behind a frozen permitting process. The constraint on AI deployment has moved from capital, to chips, to inference costs, and now to government authorization. The scarce input is no longer silicon. The scarce input is permission.

Three prior MindCast analyses anticipated the event’s shape. The Power Stack (March 2026) forecast that governments would intervene in the AI buildout only after grid problems produced visible reliability risks or visible consumer costs — Hochul’s two stated reasons. The same series forecast the state-by-state split now visible between jurisdictions that attract data center capital and jurisdictions that repel it. The Federal-State AI Infrastructure Collision (January 2026) forecast New York’s specific posture: conditioning rather than blocking, extracting terms while preserving room for investment. The record appears once, here, for one purpose — it disciplines the fourteen new dated, falsifiable predictions this paper adds.

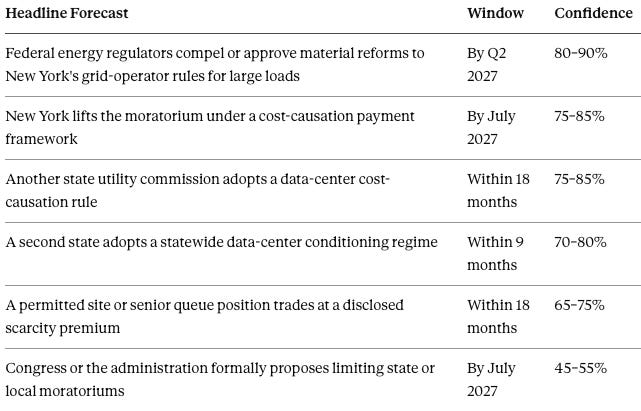

Six headline forecasts preview the full fourteen-entry register in Section XII — each carries a deadline, a confidence band, and a condition that proves it wrong:

Four findings anchor the analysis. First, EO 62 is a bargaining tool, not a ban: the order publishes its own exit price (a grid fund), exempts every approved project, and was issued by a governor moving faster than her own legislature to keep the framework’s design in her hands. Second, moratoriums mint windfalls: a permit is a real option — the right to build capacity competitors must still wait for — and every existing New York permit appreciated overnight when new approvals froze, which is why incumbent operators will fight these rules far less hard than outsiders expect. Third, the market is mispricing the entire sector by category: investors assign software multiples to companies increasingly constrained by infrastructure economics, hyperscalers have become sum-of-the-parts valuation problems spanning five economic regimes inside one ticker, and reclassification alone — no earnings change required — moves the price. Fourth, the regulation is layered and contradictory by design: the federal executive accelerates federal permitting, FERC now presses regional grid operators to reform large-load transmission rules, states condition physical siting, and cities impose their own pauses. The strictest non-preempted rule within each government’s lawful domain controls — a coordination tax that centrally governed competitors like China never pay.

The politics follow measurable rules, not noise. Moratoriums come from politically safe states first, and their spread is tracked by one variable: union posture, not environmental sentiment, because environmental opposition is universal and predicts nothing while labor decides whether a governor survives the “job-killer” attack. Behavioral economics explains the local pattern that cost-benefit analysis cannot: residents weigh feared losses — water, higher bills — roughly twice as heavily as promised gains, which is why data centers keep losing county votes even where the tax math overwhelmingly favors them, and why the winning developer strategy is guarantees against losses, not promises of benefits.

MindCast takes a position, and it cuts both ways. The industry is right on the economics: some of the largest operators already fund dedicated generation and long-term supply voluntarily — constraint-removal spending that expands available capacity — and a willing payer facing a closed path can signal a policy failure rather than a corporate one. The regulators are right on the goal: data centers should pay their own infrastructure costs, a principle that now has both a Democratic executive order and a Republican bill behind it. The correct instrument follows from both: charge them, don’t pause them. The paper closes with a five-plank model state framework — cost-causation tariffs, one threshold per state with guaranteed local consent, statutory shot clocks, an incumbent windfall check, and water-and-queue hygiene — evaluated by a single test: does the rule increase or decrease the number of places a project can viably be built?

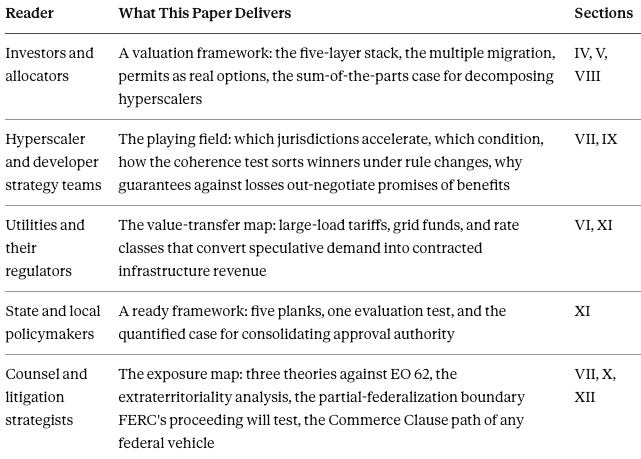

The paper serves five readers at once, and each can navigate directly to their sections:

The forecast, in one term: conditional acceleration. AI infrastructure proceeds where developers accept differentiated tariffs, prepay grid costs, secure local consent, or route through private power — and stalls where those terms are unavailable or unpriced. Fourteen predictions with deadlines, confidence bands, and falsifiers put that forecast on a public scoreboard through July 2028. The first generation of AI winners accumulated GPUs. The second accumulated inference demand. The third will accumulate megawatts — and the permission to use them.

I. The Fourth Cycle

Repricing cycles follow a recognizable sequence. Markets misprice a scarcity, an outside event exposes the mistake, and valuations reorganize around the newly recognized constraint. Each of the first three AI repricing cycles ran that sequence on a different input, and reading them in order shows why a fourth cycle was coming regardless of what New York did.

Cycle one repriced capital: markets discovered that frontier AI required investment on an industrial scale, not a software scale. Cycle two repriced compute: graphics processing unit (GPU) shortages, not engineering talent, became the main limit on who could compete. Cycle three repriced inference: serving billions of requests created permanent operating costs, and the old software assumption — that serving one more customer costs almost nothing — stopped holding.

Cycle four reprices authorization. Grid capacity, environmental review, permitting timelines, water rights, and political acceptance now determine how fast a company can deploy, alongside model quality and chip supply. The competitive advantage is shifting from firms that can buy hardware to firms that can obtain permission to use it.

Prior MindCast work anchors the claim rather than decorating it. The Power Stack (March 2026) forecast government intervention arriving only after grid problems produced visible reliability risks or consumer costs, and forecast a sharp state-by-state divergence in permitting posture within eighteen to thirty-six months (The Power Stack; The AI Infrastructure Energy Opportunity Landscape). Hochul’s stated rationale and the jurisdiction map documented in Sections VI and VII track both forecasts. The prior record matters for one reason only: it holds the new predictions in this paper to a scoring standard the reader can verify.

One question determines whether markets treat New York as an isolated political story or as the template for a national repricing: how does the order actually work? Section II reads the instrument itself.

II. Anatomy of EO 62: A Pause on Permits, Not a Ban

Precision matters here, because the popular headline — “New York bans AI data centers” — describes the order wrong, and the wrong description produces the wrong investment conclusion. An investor pricing a ban assumes capacity is destroyed. An investor pricing a conditional pause assumes capacity is delayed and a new cost is coming. The order’s text supports the second reading.

EO 62 works as a permitting pause, not a prohibition. The Department of Environmental Conservation (DEC) must hold all permit applications for data centers of 50 megawatts or more — without approving or denying them — until the Department of Public Service (DPS) completes a Generic Environmental Impact Statement (GEIS), a study covering energy demand, water use, and air quality. In plain terms: applications sit in a drawer until the study is done and rules are written.

The scale of what sits in the drawer is measurable. Nearly 12 gigawatts of data center power requests are waiting in the New York Independent System Operator (NYISO) interconnection queue — the waiting list for permission to connect large facilities to the grid — and more than 8 gigawatts of those requests arrived in 2025 alone. Twelve gigawatts is roughly the output of twelve nuclear reactors. All of that demand now waits on a paused permitting process.

Three features of the order show that it is designed as a bargaining tool, not a shutdown — confidence 80–85%:

The order names its own exit. Hochul said the moratorium lifts once the state adopts a policy requiring data center operators to pay into a statewide grid fund, and she expects that within a year. A moratorium that publishes its own price is an opening offer in a negotiation.

Existing projects are exempt. Projects already approved can proceed. Only new applications wait. Companies that already hold permits keep everything; their would-be competitors stand in line.

The governor moved before her own legislature. Last month the state legislature passed a stricter bill — a 20-megawatt threshold, new utility rate categories, mandatory public hearings — which Hochul has not signed. Her office called the executive order the fastest way to act while the bill is reviewed. By moving first, she kept control of the framework’s design: the 50-megawatt line and the grid-fund idea are hers, not the legislature’s.

Taken together, the three features describe a state trying to set terms, not stop construction: a published exit price, protected incumbents, and a framework kept in the governor’s hands where she can trade it. A bargaining tool only works, though, if the politics behind it hold — and the deeper question is why a state government now believes it has the standing to set terms for AI at all. Section III argues the answer is a change in what kind of thing AI is treated as.

III. The Infrastructure Identity Shift

Regulation follows classification. For twenty years, the decisive question about any technology company was a software question: does the business grow cheaply, with network effects and little physical footprint? Regulators looking at AI in 2026 ask none of that. They ask whether a facility overloads the grid, raises electric bills, drains water supplies, or threatens regional reliability. Those are the questions governments have always asked about power plants and pipelines — not about software.

AI did not become a utility, and the loose version of the identity-shift argument misleads on exactly that point. Foundation models still behave like software businesses, and no one is imposing public service obligations on a chatbot. What changed is narrower and more consequential: governments now regulate the physical production of AI — the buildings, the power draw, the water — using the legal machinery built for utilities and critical infrastructure: environmental review, grid connection proceedings, rate cases, siting boards, and moratoriums. EO 62 states the reclassification in its own text. The order defines a regulated data center by its power draw, cooling density, and continuous operation. What the facility computes is irrelevant. How much power it consumes is everything.

Two consequences follow, and both change what AI companies are worth. First, AI infrastructure starts behaving like a regulated network industry. Waiting lists, not markets, allocate access to the grid. Rate proceedings divide up the costs. Expansion needs a commission’s approval. Administrative hearings settle disputes, and experience with the process is itself an advantage. Companies that won by shipping products faster now compete in venues where the winning skills are rate-case advocacy, community negotiation, and queue management. Second, political capital becomes a real input to production. A company’s ability to build its next gigawatt depends on its relationships with governors, utility commissions, and host communities. Political capital appears on no balance sheet, builds slowly, does not transfer between markets, and can lose its value overnight when the politics shift — confidence 75–85%.

The identity shift does not hit every part of the AI business equally — and the unevenness is the next insight. Some layers of the industry still run on pure software economics while others already answer to utility commissions. “AI” no longer names a single kind of business. Section IV takes the industry apart layer by layer.

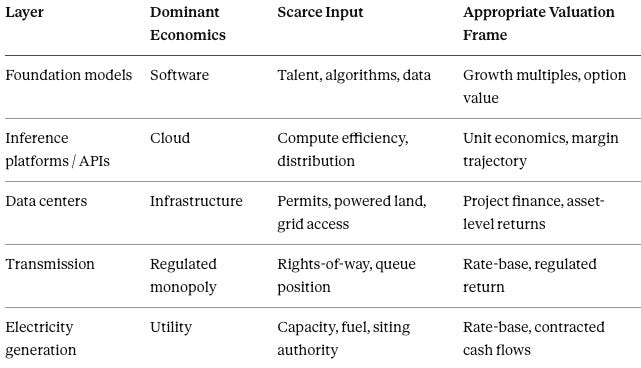

IV. The AI Stack Under Divergent Economics

Markets still discuss “AI” as if it were one kind of asset. It is now at least five, and each obeys different rules. The table below separates the layers, names the input that limits each one, and identifies how each should be valued.

Three implications turn the table above from a taxonomy into a repricing argument. First, companies that span several layers get valued at a blended average that hides where the value actually sits. A hyperscaler contains a software business, a cloud business, and a large unregulated infrastructure portfolio inside one stock ticker — and EO 62 just raised the risk on the third without touching the first two. Second, grid access itself is becoming a strategic asset. A senior position in an interconnection queue, or rights to transmission capacity, can now be worth acquiring for its own sake — the pattern MindCast documented in the Chevron–Microsoft Kilby analysis, where the companies chose Texas specifically because its grid sits outside federal jurisdiction. Third, utilities are becoming indirect AI companies. They control an input AI cannot function without, and New York’s grid-fund model would turn serving data centers from a cost problem into a revenue line.

The table also makes regulatory delay measurable rather than anecdotal. Permitting timelines, study completion dates, and queue depths are all dated, countable quantities. They belong inside financial models the same way factory construction timelines sit inside semiconductor models: as explicit variables, not as a risk disclaimer. Analysts will follow the money here — expect banks and rating agencies to start publishing state-by-state permitting metrics for data center exposure, a development the prediction register tracks below.

Divergent economics across layers points directly at a valuation question the market has put off: what happens to the price of these companies when investors finally value each layer by its own rules instead of by the blended average? Section V follows the money.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. We specialize in predictive simulations for Complex Litigation, Innovation Economics and Geopolitical Risk Intelligence.

To test our predictive simulation AI system, in 2026 we simulated the Super Bowl and the World Cup. See Super Bowl LX — AI Simulation vs. Reality | Predictive Game Theory + Behavioral Economics Cognitive Digital Twin Foresight Simulations in the World Cup

To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

V. The Multiple Migration: AI as a Regulated Asset Class

Valuation habits change more slowly than the economics underneath them, and the gap between the two is where investors gain or lose. Markets learned over decades to pay different prices for different kinds of business: software trades at high multiples because it grows cheaply, utilities trade at low multiples because regulators cap their returns, and infrastructure sits in between. Those differences are not arbitrary — they price growth, regulatory exposure, capital intensity, and certainty of cash flow. The financial core of the fourth cycle fits in one sentence: markets have been assigning software multiples to companies increasingly constrained by infrastructure economics, and correcting that mistake does not require earnings to change at all. Reclassification alone moves the price.

The multiple correction will not fall evenly across companies, and permits are the reason why. A data center portfolio that once borrowed its parent company’s software multiple now answers infrastructure questions — permit timelines, rate proceedings, grid-fund payments. Investors value an asset according to the rules it operates under, not according to the logo on the building. EO 62 changed no company’s revenue. It changed which rules a growing share of hyperscaler capital operates under.

Permission itself now carries a market price, and finance already has a name for assets like this: real options. A real option is the right — without the obligation — to take a valuable action later. A completed permit is exactly that: the right to build capacity that competitors must still stand in line for. When New York froze new permits, every existing permit in the state became more valuable overnight. Not because those sites produce anything more — but because getting a new permit went from a predictable process to an indefinite wait, and scarcity raises the price of what already exists. Grandfathering clauses guarantee this effect: every moratorium passed so far exempts already-approved projects, so every moratorium hands a windfall to the companies it exempts. One practical prediction follows: expect incumbent operators to fight moratoriums far less hard than outsiders assume, because rules that block their competitors enrich them. And expect the windfall to show up in prices — permitted sites and senior queue positions trading at visible premiums within 18 months — confidence 60–70%.

The Power Stack series supplies the vocabulary for what a moratorium does to these assets, and it exposes a loop worth stating plainly. The series divided infrastructure capital into two kinds: constraint-removal capital, which expands the system — new transmission, more transformer production, new generation — and choke-point capital, which captures existing scarcity without adding capacity. A moratorium performs a conversion no market could perform on its own: by freezing new supply, it turns every incumbent position into choke-point capital by government act. The same series argued that choke-point rents are precisely what attract the next round of regulatory attention. Put the two together and the fourth cycle feeds itself: regulation creates scarcity, scarcity creates rents for the exempted, and visible rents invite the regulation after that. New York’s moratorium is not the end of a regulatory sequence. It is a generator of the next one — most plausibly, scrutiny of the very incumbents its grandfathering enriched — confidence 55–65% that exempted-incumbent advantage becomes an explicit regulatory or antitrust topic within 24 months.

Hyperscalers now present investors with a decomposition problem. A single company like Microsoft contains a software franchise, a cloud platform, a frontier-model partnership, a global data center construction program, and a growing portfolio of power contracts — five businesses spanning every row of the Section IV table, each deserving its own discount rate. The single blended stock price hides what happens inside: a moratorium or a rate case can reduce the value of the infrastructure segment without changing reported earnings at all. Regulatory events now reprice segments while the market still quotes tickers. Sum-of-the-parts analysis — valuing each division separately, the way analysts treat industrial conglomerates — becomes the right tool for technology companies for the first time. MindCast’s Microsoft repricing analysis set a specific test date for that claim: the company’s July 29 earnings report, where infrastructure-scale spending meets software-multiple expectations inside one document. The explicit conclusion for investors: expect the largest AI companies to trade increasingly like conglomerates, where regulatory news moves the value of one division while the ticker responds slowly and imprecisely.

One consequence of the migration cuts against the pessimistic reading, and it deserves plain statement. A regulated multiple is not simply a lower multiple. Regulation trades growth for certainty, and certainty has wealthy buyers: pension funds and sovereign wealth funds pay premium prices for steady, commission-governed cash flows. The likely endgame of this migration is not cheaper AI companies but restructured ones — infrastructure divisions spun off to investors who want regulated returns, while the software divisions keep the multiples they still earn. The data center real estate investment trust (REIT) already proves the model works — confidence 65–75%.

Once classification drives valuation, whoever controls classification controls the repricing. Governments now hold that power, which is why the rest of this paper is about politics and geography rather than models and chips. Section VI asks which governments moved first, and why.

VI. The Political Economy: Who Moves First, and Why

A regulation travels only as far as its political cover extends, so the identity of the first mover tells you a great deal about where the regulation goes next. New York’s moratorium came from a specific political position — a secure incumbent acting where more cautious peers declined — and reading that position correctly turns one state’s decision into a forecast.

Moratoriums come from politically safe states first. Hochul signed EO 62 while leading her Republican challenger by roughly 20 points. She acted where fellow Democratic governors declined: Maine’s Janet Mills vetoed her own legislature’s moratorium over a missing exemption for one project, and Virginia’s Abigail Spanberger has not moved. Fourteen state legislatures have introduced data center restriction bills; before Tuesday, none had become law. The prediction that follows: the copycat wave runs through Democratic states with strained grids and safe incumbents, not through swing states competing for the investment — confidence 65–75%.

A second signal matters more for forecasting: the Democratic coalition split in public on day one. The president of the plumbers and pipefitters union condemned the moratorium as a job-killer. Environmental groups praised it. Senator Bernie Sanders and Representative Alexandria Ocasio-Cortez used it to push for a national pause. A one-party split between labor and environmentalists is genuinely useful information, because it predicts which states can hold a moratorium politically and which cannot.

A third fact complicates the partisan story, and it strengthens the paper’s thesis. The principle that data centers should pay their own infrastructure costs is not a Democratic idea — it now has a Republican bill. Representative Michael Baumgartner of Spokane, whose Eastern Washington district is courting data centers for its cheap hydropower, has introduced the Power and Water for Families Act: a national framework requiring any large new facility to pay the full incremental cost of the generation, transmission, and grid upgrades it causes, to post financial guarantees so ratepayers are not left holding speculative projects, and to use recycled water rather than drawing down aquifers, supported by a new tax credit for water-reuse systems. His stated principle — “If you build it and use it, you should pay for it” — is Hochul’s grid fund translated into Republican language, wrapped in an argument that America must beat China in AI. The partisan line therefore sits in a different place than the moratorium map suggests. The parties disagree about pausing construction. A working consensus is forming, across both parties, that data centers should pay for their own grid impact. Cost-allocation rules are becoming the bipartisan center of this debate, which raises the odds on the register’s grid-fund predictions.

One more force operates above state politics: the national press. On July 14 — the same day Hochul signed the order — The Atlantic published “Generative AI Is an Engineering Disaster,” arguing that the AI buildout pushes its costs onto ordinary consumers, with data centers buying up to 70 percent of the world’s high-end computer memory and hardware prices rising as a result. AI researchers disputed the article’s engineering claims within hours, and the piece belongs to an announced investigative campaign, so its technical accuracy should be treated as contested. The industry’s counter-narrative also has evidence behind it: the largest operators are financing new generation — restarted nuclear plants, new geothermal — which adds electricity supply to the system rather than merely consuming it, a fact the cost-externalization story omits. But the narrative’s political effect does not depend on which side is right. “AI raises your bills” now runs through two channels at once — electric rates and hardware prices — and a cost story with national-magazine reach lowers the political cost of intervening everywhere at the same time. The Power Stack predicted that visible consumer costs would be the trigger for government action. The trigger condition now publicly exists — confidence this accelerates the propagation predictions AIRC-III-2 and AIRC-III-7: 60–70%.

The politics of this section reduce to one practical monitoring rule: watch the unions, not the environmental groups. Environmental opposition to data centers is nearly universal, so it predicts nothing. Union positions differ state by state, and they decide whether a Democratic governor can survive the “job-killer” attack that follows a moratorium. Washington’s legislature already ran the play the model predicts: its data center bill attached prevailing-wage, apprenticeship, and project-labor-agreement requirements to any behind-the-meter generation an operator builds — the legislative purchase of building-trades support, written directly into the framework. States where the building trades stay neutral or supportive are the candidate list for the next moratorium. Politics draws the map — and Section VII reads that map, level of government by level of government.

VII. Regulatory Geography: The Vertical Stack and the Horizontal Map

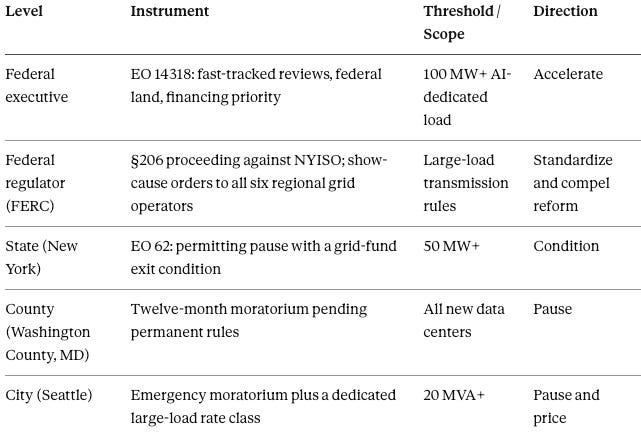

Semiconductor manufacturing taught the technology industry a lesson software never had to learn: when production is physical, geography is strategy. AI deployment now runs the same lesson along two axes at once. The horizontal axis asks which state a company builds in. The vertical axis asks how many levels of government must say yes. New York is the model for the first question. Washington State is the model for the second.

The vertical stack. Data center approval now runs through four levels of government — federal, state, county, city — but federal authority itself divides into two distinct channels. The executive branch accelerates federal permits and federal-land routing. Executive Order 14318 (July 2025), issued alongside the administration’s AI Action Plan, directs agencies to streamline environmental review, expedite water permits, offer federal land, and fast-track qualifying projects of 100 megawatts or more. The Federal Energy Regulatory Commission (FERC) governs a different layer: the rates, terms, and conditions of interstate transmission service. Congress holds the remaining policy positions. Sanders and Ocasio-Cortez propose a national pause; Baumgartner proposes national payment conditions. Acceleration, pause, and conditioning are therefore all live federal postures.

Beneath the federal level, the siting brakes stack. New York pauses state permits at 50 megawatts. Washington County, Maryland adopted a twelve-month county moratorium on July 1 after residents raised water and grid concerns. Seattle’s city council voted unanimously on June 9 to freeze new data center siting for a year at 20 megavolt-amperes (MVA) — less than half New York’s threshold — while creating a dedicated electricity rate category for large Seattle City Light customers.

Federal intervention has already begun. On June 18, 2026, FERC issued Federal Power Act §206 show-cause orders to all six regional grid operators, including NYISO, requiring them and their transmission owners to justify their existing large-load tariffs or propose reforms. FERC identified five reform categories: faster and more efficient transmission-service studies, protection against cost shifting, rules for co-location and behind-the-meter generation, flexible transmission products for large loads, and coordinated study of generation serving electrically proximate or co-located loads. NYISO now sits inside an active federal proceeding, Docket No. EL26-69-000, while New York’s environmental permitting pause remains in force.

The division of authority is the finding. FERC expressly preserved state authority to select, site, and permit generating resources and state public utility commission authority over retail electricity rates. FERC can change how quickly, at what transmission price, and under what service conditions a large load reaches the interstate grid. FERC cannot presently compel New York’s environmental agency or a city planning board to approve the physical site. The governing rule is therefore not that the strictest layer always wins. The strictest non-preempted layer within its lawful domain controls: FERC may dictate the transmission pathway and its price, while states and municipalities still control much of the place where the pathway terminates. Three governments now define the regulated object at three different sizes — 100 megawatts federally, 50 in New York, 20 megavolt-amperes in Seattle — and threshold fragmentation is itself a compliance cost software companies never carried.

One table summarizes the full stack — five layers of government, four directions of pressure, and no two using the same definition of the regulated facility:

FERC’s action moves MindCast’s partial federalization forecast from theory to operating fact. The Federal-State AI Infrastructure Collision (January 2026) predicted that federal authorities would gain control over process while states retained control over place and cost, that consumer-protection framing would become the standard state response, and that New York would condition rather than prohibit investment. FERC now federalizes the transmission process; EO 62 conditions the physical site and cost allocation. Neither actor controls the whole pathway. Commissioner Laura Swett LaCerte’s NYISO concurrence underscores the likely trajectory: region-specific proposals first, broader use of FERC’s transmission jurisdiction if NYISO fails to respond adequately. The concurrence is not a binding Commission holding, but it reveals the enforcement posture behind the proceeding.

The federal intervention ladder has four rungs. First, FERC can standardize or compel transmission tariffs, large-load studies, flexible service, co-location rules, and cost allocation under the Federal Power Act. Second, the President can accelerate federal reviews, federal land, financing, and agency priorities under existing statutes, but an executive order cannot erase state zoning or environmental law by declaration alone. Third, Congress can create a federal siting or large-load regime and expressly preempt conflicting state requirements under the Commerce Clause, provided the federal law regulates private conduct or establishes a federal standard rather than commanding state legislatures to repeal their own laws. Murphy v. NCAA marks that boundary between valid preemption and unconstitutional commandeering. Fourth, private litigants can invoke the dormant Commerce Clause, but EO 62’s facial neutrality and conventional local purposes — reliability, water, air quality, and ratepayer protection — make a clean constitutional victory less likely than a narrower state-law or administrative challenge. The durable federal design remains the one MindCast’s Commerce Clause analysisrecommends: absorption, not erasure — national transmission and cost-causation standards that federate useful state experiments while leaving genuinely local siting questions local.

The split carries a measurable coordination tax. Every additional authority adds study time, negotiation cost, and the possibility that one approval arrives after another expires. China can direct grid expansion, generation siting, and load allocation through a far more centralized hierarchy; the United States pays for pluralism at several desks. The tax is not an argument against ratepayer protection. It is the reason instrument design matters. Rules that price access collect protection while keeping pathways open. Rules that close pathways collect similar protection at a much larger cost in delayed investment and national competitiveness.

The coordination tax also has a temporal structure. The National Innovation Behavioral Economics (NIBE) framework estimates a mismatch of roughly five to one: markets move in 12-to-24-month cycles, governing institutions in 3-to-7-year cycles, and infrastructure in 10-to-15-year cycles. The ratios rest on observable public baselines, not internal assumptions. Chip generations and frontier-model releases turn over in one to two years. A full federal environmental impact statement has averaged roughly four and a half years to complete, according to the Council on Environmental Quality’s own timing studies. Major interstate transmission lines routinely take a decade or more from proposal to energization — SunZia and TransWest Express each spent well over fifteen years in development before construction began. The full calibration methodology behind the metrics sits in the NIBE publication and MindCast engagement materials; this paper uses only the ratio’s direction, which the public baselines independently support. Federal transmission reform can compress one part of the mismatch, but it cannot eliminate state environmental review, municipal land use, or construction time. Conditional acceleration therefore becomes more likely than either complete federal takeover or unconditioned deployment.

Two directions of flow. New York and Washington State show opposite mechanics, and the difference predicts what other states will look like. New York regulated from the top down: a governor moved before her own legislature, imposed one statewide framework, and left local zoning intact beneath it. Washington regulated from the bottom up, by accident — and the legislative record shows how close the state came to acting. House Bill 2515 passed the House 51–41 on February 14 and cleared the Senate policy committee with amendments, then died without a vote in Senate Ways & Means when the session adjourned on March 12. Its Senate companion, SB 6171, ran the same course: the policy committee advanced it 7–4 on party lines, and Ways & Means never voted. A framework that survives every policy test in both chambers and dies at both fiscal gates is a stall, not a rejection — the choke point was the fiscal note, not the idea. Governor Ferguson’s Data Center Workgroup will not deliver replacement legislation until 2027, and into that vacuum stepped Seattle’s city council, within weeks of four companies approaching City Light with five large proposals. Seattle joins Denver, Baltimore, Atlanta, Minneapolis, and at least three other Puget Sound jurisdictions with similar measures. The general rule: where a state acts, local rules harmonize under one framework; where a state stalls, cities improvise — and companies inherit a patchwork with lower thresholds and shorter fuses than any statehouse would have set — confidence 70–80%.

The horizontal map. Across states, the sorting runs between places that compete on speed and places that compete on terms. Texas competes on speed by legal design: its grid operator, the Electric Reliability Council of Texas (ERCOT), sits largely outside federal jurisdiction, which is exactly why the Chevron–Microsoft Kilby project chose it. Virginia competes on speed through incumbency: Data Center Alley’s existing substations, fiber, and experienced permitting offices compress timelines even as local resistance grows. Georgia recruits actively, and New York’s own contractors named Virginia, Texas, and Georgia as where the paused projects will go. The conditioning states set prices instead of blocking: New York through grid funds and community consent; Maine through Mills’s chosen combination — veto the moratorium, but strip data centers of tax breaks; Anchorage through a permitting framework that ties approval to demonstrated utility capacity. Washington State is becoming the most instructive case because both parties are conditioning it at once: Seattle pauses from the left over grid and rate concerns, while Baumgartner conditions from the right over ratepayer costs and the Spokane aquifer — cheap Grand Coulee hydropower attracting the industry, and both parties insisting the industry pay its own way in.

The end point of the regulatory progression deserves its own sentence: AI is becoming land-use economics. Follow the chain of constraints to the end and deployment turns on none of the inputs the industry celebrates — not algorithms, not GPUs, not even electricity in the abstract — but on zoning variances, wetlands reviews, county planning commissions, and community hearings. A trillion-dollar industry now competes, at the margin, in front of county planning boards. And the boards know it: Washington County’s pause and Seattle’s 20 MVA line were drawn by local officials who understood, correctly, that they hold veto power over the most valuable companies on earth. The pattern has precedent — railroads were constrained by rights-of-way, telephone companies by franchise agreements, nuclear plants by siting boards. Each time, land — the oldest asset class in economics — ended up constraining the newest industry.

The paper’s causal chain is now complete, and it reads in one sequence: the identity shift decides which questions regulators ask, the stack decides which economics apply, politics decides which governments ask hardest, and location decides who absorbs the answer. Section VIII names who wins and who loses.

VIII. Winners and Losers

Every repricing redistributes value before it destroys any, and this one follows the pattern. EO 62 did not eliminate the underlying demand for AI capacity. It delayed, redirected, or repriced where that demand can be served, raised the value of permissions already granted, and created new income for whoever owns the assets the pause cannot touch.

Winners. Operators with completed permits in New York now own a state-enforced advantage: their approved capacity gained scarcity value the moment new approvals froze. Owners of powered land, long-term power contracts, and senior grid-queue positions in other states gained relative ground, because those assets are now understood as the options described in Section V. Recruiting states gain directly — New York’s contractors expect the paused projects to land permanently in Virginia, Texas, and Georgia. Regulated utilities gain most durably. They control an input AI cannot function without, and the grid-fund model turns big data center customers from a cost-sharing headache into a dedicated revenue category.

Losers. Developers who depend on building new sites from scratch take the direct hit, along with every NYISO queue position that lacked a completed application on July 14. A less obvious loser: New York’s own semiconductor recruitment. The state spent years attracting chip factories with subsidies and grid commitments, and a rule that regulates any facility by its power draw catches fabs in logic written for data centers. Expect that contradiction to surface publicly within six months, most likely as a fight over an exemption — confidence 60–70%.

The winner-loser pattern is the paper’s clearest investment finding. Winners hold physical and political assets — permits, powered land, queue seniority, regulator relationships. Losers hold financial and technical assets — capital, designs, and places in a frozen line. Cycle four marks the first category up and the second category down. Before turning that into dated predictions, Section IX explains the strategic mechanism behind that sorting, Section X states what would prove the whole argument wrong, Section XI states where MindCast stands, and Section XII prices what survives.

IX. The Game-Theory Read: Regulation as a Game Replacement

The sorting of winners from losers in Section VIII has a strategic mechanism underneath it, and MindCast’s Dynamic Predictive Game Theory (DPGT) framework names it precisely. Classical game theory assumes the rules stay fixed while players choose strategies. DPGT studies the contests that actually occur, where a single event — a court ruling, a rate decision, a regulatory intervention — does not change a variable inside the game but replaces the game entirely: new payoffs, new available moves, a new value on time. EO 62 is a textbook game replacement. On July 13, the game in New York was “who builds fastest.” On July 14, it became “who negotiates the exit terms” — and every strategy optimized for the first game lost value overnight.

A replaced game changes what winning means. In a fixed game, the winner is the actor with the best strategy. In a game that keeps getting replaced, the winner is the actor whose decision-making system stays coherent across the replacements — the condition MindCast calls Adaptive Coherence Equilibrium (ACE). Coherence is not stubbornness: a developer still running the greenfield playbook after July 14 is not coherent, it is rigid, and rigidity in a changed game is how value gets destroyed. A coherent actor changes strategy the moment the game changes while remaining recognizably itself — same capabilities, same institutional identity, new play. The question that predicts the next two years of this industry is not “who has the best model” or even “who has the most megawatts,” but “whose decision architecture holds when the rules move again.”

Applying the coherence test to the winners and losers of Section VIII explains the sorting without any new facts. Regulated utilities hold coherence effortlessly — not because they adapted well, but because the game moved onto their home field: rate cases, commission hearings, and cost allocation are the game they were built for, so a rule change that forces everyone else to learn utility procedure is, for them, no change at all. Hyperscalers with standing permitting teams, political relationships, and routing options — dedicated generation, friendlier jurisdictions — hold coherence at a cost. Greenfield developers built for one game — find land, build fast — face the hardest test, because their entire architecture assumed rules that no longer exist. Speed of adjustment is measurable, and it will show in the public record: the firms that reposition within weeks of EO 62 capture the option value described in Section V, while the firms that wait for legal clarity watch the window close.

Behavioral economics explains the part of this story that cost-benefit analysis cannot: why data centers keep losing local votes even where the tax math favors them. Loss aversion — the finding, from Daniel Kahneman and Amos Tversky’s prospect theory, that people weigh losses roughly twice as heavily as equal gains — runs through every level of the record this paper assembles. Residents at a planning-board hearing weigh feared losses (water, higher bills, a changed town) more heavily than promised gains (jobs, tax revenue), which is why Loudoun-style tax arguments underperform at podiums and why Washington County’s commissioners voted 4–1 against a $57 billion pipeline of statewide investment. Governor Mills’s veto in Maine follows the same logic from the opposite side: one concrete, visible project loss in the town of Jay outweighed diffuse statewide risks. And the incumbents’ silence follows it too — companies now holding scarce permits behave exactly as endowment effects predict, quietly protective of a windfall they never had to argue for.

Loss aversion also operates inside the permit office, and it explains why delays persist even where no one opposes a project. MindCast’s NIBE work measures what it calls the Risk Interpretation Index: the mid-level reviewers who control actual approval timelines systematically overweight approval risk, because an approved project that later fails can damage a career, while a delay carries no penalty at all. The federal-scale demonstration came from the White House Genesis Mission analysis, which found that repairing those mid-level incentives accelerates deployment roughly three times more than adding senior political oversight does. The finding carries directly into this paper’s framework: plank three’s shot clock works not because it hurries anyone, but because it finally gives delay a cost — correcting the one-sided incentive that makes slow the safest thing a reviewer can be.

Loss aversion also explains why the model framework in Section XI is built the way it is. Cost causation works politically, not just economically, because it removes the feared loss instead of promising a compensating gain: a resident guaranteed that their rates cannot rise needs no persuading about tax revenue. Developers who lead with guarantees against losses — rate protection, water commitments, the financial assurances in Baumgartner’s bill — will out-negotiate developers who lead with promised benefits, and states that write loss-protection into statute will site facilities that states relying on benefit-promises cannot. The behavioral read and the game-theory read converge on the same forecast: the fourth cycle rewards the actors who understand which game is now being played, and in the new game the currency is protection, not promises. Section X states what would prove all of this wrong.

X. What Would Falsify the Thesis

A framework earns credibility by naming its own failure modes before critics do. The regulatory repricing thesis has four. Each is described plainly below, with a probability, and the prediction register in Section XII inherits their conditions. Naming them also clarifies what this paper does not claim: it does not claim the AI buildout stops, and it does not claim every moratorium survives.

Failure mode one: courts strike or narrow the model. EO 62 pauses permits statewide by executive order, without new legislation. An order of that shape invites three principal theories: the governor exceeded delegated authority under New York law; queue holders or applicants suffered a compensable deprivation; or the pause imposes an unconstitutional burden on interstate commerce. The dormant Commerce Clause claim is plausible but not the cleanest path. EO 62 appears facially neutral and invokes conventional local interests — reliability, water, air quality, and ratepayer protection — so a challenger would need unusually strong evidence of protectionist design or a burden clearly excessive relative to those benefits. A statutory-authority or administrative-law claim may therefore reach the merits sooner.

One Commerce Clause theory deserves fuller treatment than the standard analysis gives it: extraterritorial effects. Data centers are not local businesses that happen to be large; they are nodes in inherently interstate markets. New York capacity serves cloud customers, financial-services routing, and latency-sensitive workloads across state lines, so a statewide construction pause does not stay inside state borders — it constrains supply in a national compute market and shifts traffic, prices, and siting decisions in other states. National Pork Producers Council v. Ross (2023) cuts both ways on that theory. The decision closed the door on near-automatic extraterritoriality claims: the Court upheld a California law whose practical costs fell mostly on out-of-state producers, holding that in-state regulation does not become unconstitutional merely because its economic effects travel. But the decision left Pike balancing alive — a challenger can still argue that a law’s burden on interstate commerce is clearly excessive relative to its local benefits. The strongest fact pattern for a challenger is accordingly narrow: an out-of-state cloud customer or interconnection applicant showing that New York capacity has no practical substitute for a latency-bound interstate service, and that a pause delivers little incremental local benefit over the cost-causation tariffs that could protect ratepayers without freezing supply. Even that framing runs uphill. Courts rarely strike facially neutral utility and land-use measures under Pike, and New York’s published exit condition weakens any excessive-burden story. The realistic function of the extraterritoriality theory is leverage rather than victory: pleading it raises the legal cost of extending the moratorium past its stated window — which reinforces the register’s first prediction rather than threatening it. A court striking or narrowing the order would not kill the identity-shift thesis, which now stands independently on FERC, Seattle, county, and federal-executive action, but it would end New York’s status as the model and force AIRC-III-1 to resolve early. Probability of a formal legal challenge within six months: 50–60%. Probability a dormant Commerce Clause theory is pleaded: 30–40%. Probability a Commerce Clause theory materially succeeds before the GEIS completes: 15–25%. Probability any challenge significantly narrows the order before the study finishes: 25–35%.

Failure mode two: companies route around permission instead of paying for it. Hyperscalers have countermoves the moratorium wave cannot reach: building their own power generation on site, buying campuses that already have power, using federal land offered under EO 14318, and siting in Texas, where the grid sits outside federal jurisdiction — the same combination of moves Chevron and Microsoft used when they built dedicated generation for an AI campus inside ERCOT. If routing around regulation scales faster than regulation spreads, permission never becomes truly scarce, and this repricing fades into a two-year inconvenience. Probability that routing strategies substantially blunt the repricing within 24 months: 30–40%. Note what this failure mode does not threaten: routing around regulation requires enormous capital, so only the largest firms can do it — which accelerates the sorting of winners from losers rather than preventing it.

Failure mode three: demand falls. The whole framework assumes the hunger for megawatts continues. Two things could relax the constraint from the demand side: AI models becoming efficient enough that computing needs shrink, or an investment correction that cancels queued projects before regulators ever rule on them. History leans against the first — efficiency gains have usually increased total consumption of computing, not decreased it — and 12 gigawatts of pending requests in New York alone suggests demand is outrunning efficiency for now. But the question is genuinely open. Probability that demand-side relief substantially loosens the permission constraint by 2028: 20–30%.

Failure mode four: the numbers favor the buildout. The moratorium wave is real and, so far, small. Wisconsin alone has seven major projects worth more than $57 billion moving forward. In Loudoun County, Virginia, data center taxes fund cuts to residents’ tax rates — the argument the lone dissenting commissioner made against Washington County’s pause. And a large customer with a long-term contract can lower everyone’s rates by spreading the grid’s fixed costs across more usage. Counted against total national construction, the pausing jurisdictions are a small minority. The paper’s predictions concern the trend, not today’s totals — and a reader who weighs today’s totals more heavily concludes the repricing is two or three years early, not wrong. The register exists to settle exactly that kind of dispute.

The survey changes the paper’s posture without changing its content. Regulatory repricing is the most likely outcome, not a certainty. The thesis’s strongest challenge is companies routing around regulation, not courts. The thesis’s weakest assumption is that demand stays high, not that politicians stay willing. Analysis this close to live policy also owes readers a position, and Section XI states MindCast’s.

XI. The MindCast Position and a Model Framework

Analysis that stops at description ducks the question every reader of this paper will ask: are New York and Washington doing the right thing? MindCast’s answer follows directly from the paper’s own findings, and it separates the goal from the tool.

Start with where MindCast sides with the industry, because on the economics the buildout’s case is stronger than the moratorium wave’s rhetoric admits — and three facts anchor it. First, some of the largest operators are already internalizing substantial portions of the infrastructure burden. The signature moves of the past two years include dedicated generation deals, restarted nuclear plants, newly funded geothermal, and long-term contracts that can add supply to the system rather than merely consume existing capacity. Under this paper’s own test, that is constraint-removal capital — spending that increases the number of viable deployment paths — and it is being deployed voluntarily, at private expense, by the very firms the moratoriums target. Second, the 12-gigawatt queue indicts both grid-development speed and queue governance. Some requests may be speculative, but a backlog that deep still shows that the interconnection system operates at a pace built for a slower load-growth era. Pausing demand because supply processing is slow gets the causation backwards, and no state ever fixed a slow permit office by turning away the applicants offering to fund its expansion. Third, the benefits are concrete, not promised. Where the buildout is mature, data center tax revenue funds cuts to residents’ tax rates; a large customer on a long-term contract spreads the grid’s fixed costs across more usage, which can lower everyone else’s bills; and the national stake is real — the AI race is being run whether or not any given state participates, and the compute will be built somewhere.

The industry’s position is not inferred — it sits in Washington’s official hearing record, where the Data Center Coalition testified that the industry is “fully committed to paying full costs” and to protecting other customers from stranded assets (Senate bill report, SB 6171). The position compresses into one sentence: a willing payer facing a closed path is a policy failure, not a corporate one. The right response to a customer offering to pay the full cost of new infrastructure is to take the money and build the grid — which leaves every other ratepayer with a bigger, better-funded system. Both states get graded against that standard below.

The goal both states are reaching for is correct, and it now has a name both parties use: cost causation. A facility that requires new generation, transmission, or water infrastructure should pay the full incremental cost of it — not ratepayers, not taxpayers. Hochul’s grid fund says this. Baumgartner’s bill says this. The principle is economically sound and MindCast endorses it without reservation.

The moratorium, however, is the wrong tool for that goal, and Section V already showed why. A pause hands windfalls to incumbents, invites litigation, pushes demand to Virginia and Texas rather than reducing it, and produces nothing a ratepayer can spend. Pricing achieves the same protection without the distortions. In one sentence: charge them, don’t pause them.

New York therefore gets a conditional grade: right goal, second-best tool, defensible only because the order published its own exit. If the state lifts the moratorium under a payment framework within its stated year, EO 62 will have worked as a forcing device. If the moratorium extends past July 2027, it stops being ratepayer protection and becomes a state-enforced moat for the companies that already hold permits. AIRC-III-1 in the register below is therefore not just a forecast — it is the test New York set for itself.

Washington gets a harder grade: the state stalled at the last gate, and the stall produced a worse outcome than either passing or killing House Bill 2515 cleanly would have. The House passed the bill 51–41; the Senate policy committee advanced it with amendments; the Senate fiscal committee then let it die without a vote. A near-enacted framework left a vacuum anyway, Seattle filled it, and the state now has a city-by-city patchwork with thresholds no statehouse would have chosen — bad for developers who face inconsistent rules, bad for cities negotiating alone against the world’s largest companies, and bad for ratepayers outside Seattle, who get no framework at all. MindCast’s position: Olympia should pass a comprehensive statewide framework in the 2027 session, built on cost causation, superseding the patchwork — one set of rules serving both Seattle’s grid concerns and Eastern Washington’s recruitment ambitions. Baumgartner’s payment and water-reuse principles are the right economics; whether they belong in federal or state law remains genuinely open, because one national rule fits hydro-rich Washington and gas-dependent states differently.

Criticism obligates a proposal, so MindCast offers one: a model state framework with five planks, each built to prevent one of the failure patterns this paper documents.

Plank one: charge, don’t pause. Applications keep processing under plank one; only the price changes. Any facility above the state threshold pays the full incremental cost of the generation, transmission, and grid upgrades it causes. The facility posts financial assurances before connecting. And it takes service under a dedicated large-load rate class, so its costs never blend into residential bills. Plank one combines Hochul’s fund, Baumgartner’s bill, and Seattle’s rate class into a tariff instead of a freeze — protecting ratepayers without minting incumbent windfalls or inviting lawsuits.

Plank two: one threshold per state, with local consent guaranteed by law. Three governments defining the same facility at three sizes is pure waste. The state should set a single definition and preempt local thresholds — and pay for that preemption by writing local leverage into statute: no siting without host-community approval, plus defined community-benefit, wage, and local-hire standards. Cities trade improvised moratorium power for guaranteed bargaining power. Plank two is the deal that prevents the Washington patchwork. Quantified support comes from MindCast’s own Washington analysis: the state’s seven-layer approval stack — federal power marketing, FERC, state agencies, counties, cities, public utility districts, and tribal governments — costs it an estimated $30 to $50 billion in investment lost to Texas, Virginia, and Oregon, and the highest-leverage fix identified was consolidation into a single decision point, because consolidating authority beats optimizing each institution separately.

Plank three: a shot clock, never an open-ended pause. A state that genuinely needs a study period should authorize it by legislation with a hard deadline: permits resume automatically when the clock expires unless new rules have been enacted. A deadline written into statute does what a deadline announced at a press conference cannot — survive a lawsuit and resist drift. Plank three is the direct answer to New York’s largest risk.

Plank four: the incumbent windfall check. Section V showed that every grandfathering clause enriches the companies it exempts. The fix: exempt existing projects from the pause but not from the pricing — cost-causation charges reach incumbents at contract renewal or expansion. Ratepayer protection should not double as a moat.

Plank five: water and queue hygiene. In aquifer-dependent regions, require recycled water and offer a reuse tax credit — Baumgartner’s mechanism, generalizable to any state. And require refundable deposits on interconnection requests to flush speculative applications from the queue: New York’s 12-gigawatt backlog almost certainly contains phantom projects that will never build, and no state can plan a grid around requests that exist only on paper.

The one-line version: a state that adopts all five planks never needs a moratorium, and a state already inside one has its exit ramp. New York needs planks three and four to avoid becoming the thing it claims to oppose. Washington needs planks one and two in the 2027 bill to dissolve the patchwork it accidentally created.

One test evaluates every plank — and every future rule any state proposes — at once, and it comes from the Power Stack series: does the rule increase or decrease the number of places a project can viably be built? MindCast calls that count the Geodesic Availability Ratio (GAR) — in plain terms, how many viable deployment paths exist across the system. A moratorium closes paths and fails the test. A cost-causation tariff prices paths without closing any and passes. The test resolves the apparent conflict between protecting ratepayers and staying competitive: a rule that allocates costs correctly while keeping paths open does both, and a rule that closes paths does neither for long — it just moves the projects, the jobs, and eventually the tax base to a jurisdiction that kept its paths open.

Stating a position and proposing a remedy sharpens rather than compromises the foresight record, because both concern instrument design, not partisan outcome — and the register that follows scores them. If states converge on cost-causation frameworks, the grid-fund predictions resolve true; if the moratorium wave spreads instead, the propagation predictions resolve true and the framework above becomes each new state’s exit ramp. Section XII lists the entries.

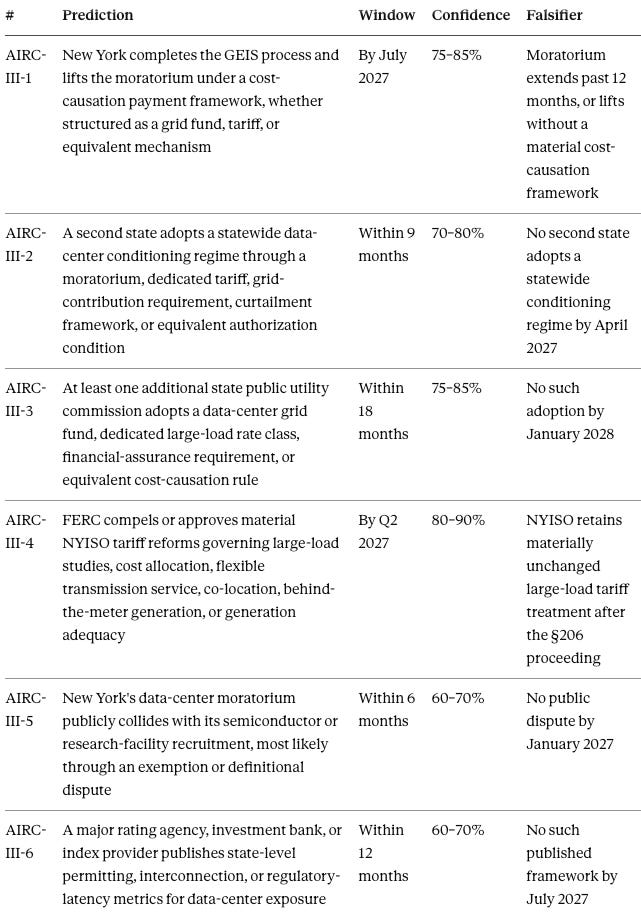

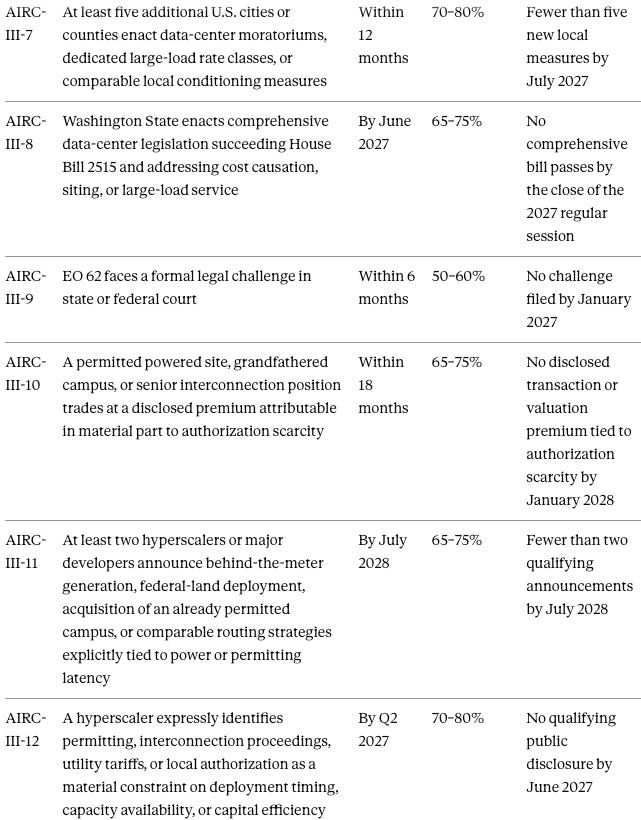

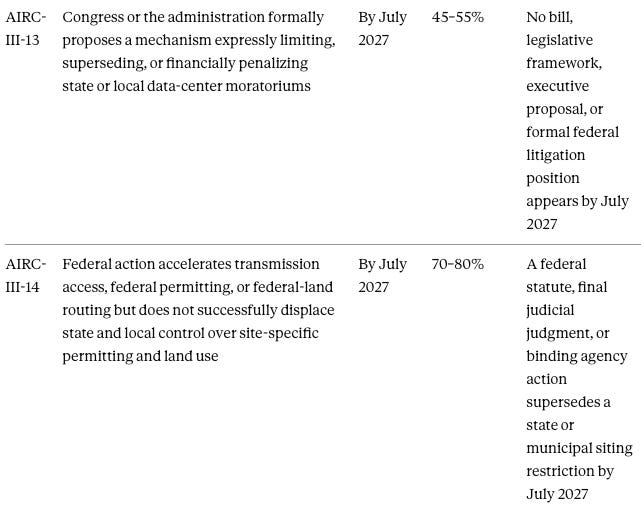

XII. Prediction Register — AIRC-III

The register uses the AI Repricing Cycle (AIRC) namespace, entries AIRC-III-1 through AIRC-III-14. MindCast publishes forecasts the way an exchange lists contracts: each entry has a deadline, a confidence band, and a condition that proves it wrong. The federal intervention changes the register’s hierarchy. FERC has already opened the large-load proceeding, so the question is no longer whether federal intervention begins; the question is what remedy it produces and whether partial federalization holds. Several entries share causal drivers: AIRC-III-1 and AIRC-III-3 depend on cost-causation convergence; AIRC-III-2 and AIRC-III-7 depend on political propagation; AIRC-III-4 and AIRC-III-14 arise from the same FERC proceeding; AIRC-III-9 and AIRC-III-13 test distinct judicial and legislative routes. The fourteen entries should

Every entry resolves from public records. The New York DPS and governor’s office decide AIRC-III-1 and AIRC-III-5; state statutes and commission dockets decide AIRC-III-2, AIRC-III-3, and AIRC-III-8; FERC Docket No. EL26-69-000 decides AIRC-III-4; published research decides AIRC-III-6; municipal records decide AIRC-III-7; court dockets decide AIRC-III-9; transaction disclosures decide AIRC-III-10; corporate announcements and filings decide AIRC-III-11 and AIRC-III-12; the Congressional Record, White House, agency notices, or federal pleadings decide AIRC-III-13; and the combined federal, state, and judicial record decides AIRC-III-14. The register remains live through July 2028, with resolutions published as they land.

XIII. Conclusion

EO 62’s own text makes the paper’s argument better than any analyst can. The order defines a data center by its power consumption, not by what it computes. When the regulator classifies an industry by megawatts, the market should value it by megawatts. New York did not invent this cycle — the queue backlog, the ratepayer politics, and the grid limits built it over two years. The executive order simply made the cycle visible, and visibility is what triggers repricing.

The end state also has a name. A companion to this paper — the AIRC-III Cognitive Digital Twin Library — models the fourteen actors who each control a portion of the authorization pathway: governors, environmental agencies, system operators, hyperscalers, developers, utilities, competing states, labor, ratepayer coalitions, investors, litigants, and analysts. No actor controls the whole pathway; several can delay it. Their interaction does not converge on a ban and does not converge on an unconditioned buildout. It converges on conditional acceleration: FERC standardizes parts of the transmission pathway, states and cities retain site-specific leverage, and large-scale AI infrastructure proceeds where developers accept differentiated tariffs, prepay grid costs, secure local consent, or route through private and federal capacity — while stalling where those terms remain unavailable or unpriced. Conditional acceleration is this paper’s modal forecast, the register is its scoreboard, and the model framework in Section XI is its recommended legal form.

Artificial intelligence has not become less valuable. Value has moved — into infrastructure economics, where permission compounds like capital and permitting expertise is worth what patents used to be. The first generation of AI winners accumulated GPUs. The second generation accumulated inference demand. The third generation will accumulate megawatts — and the permission to use them.

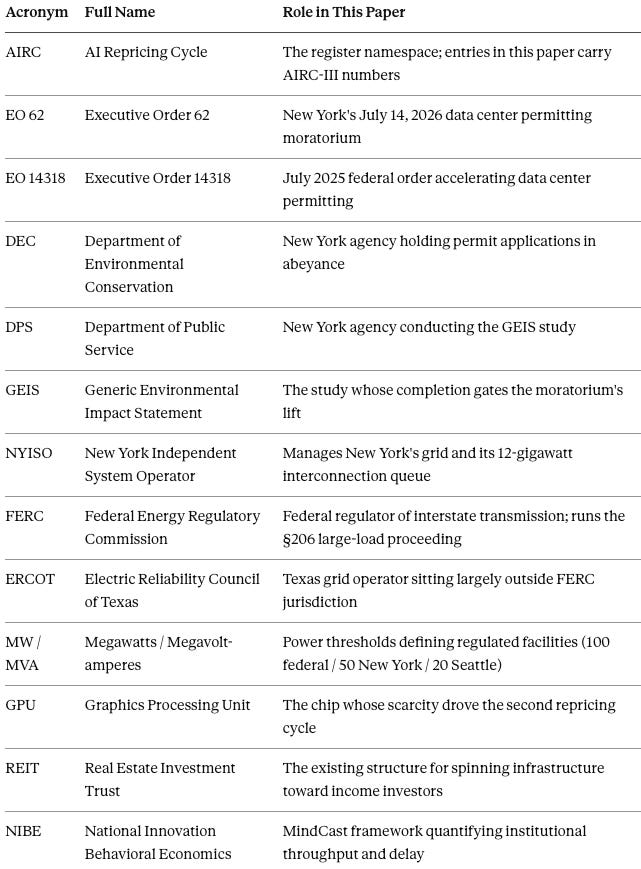

Appendix A — Acronym Reference

Appendix C — MindCast AI Works Cited

The AI Repricing Cycle

AI Repricing Cycle 2026 — Installment I — Establishes the repricing-cycle framework and documents the capital-scarcity phase that this paper extends to authorization.

Escape from the AI Repricing Cycle — Installment II — Prices the inference-cost phase and sets the July 29 Microsoft earnings checkpoint that Section V uses as a live test date.

The Inference Economy — How the TPU Bifurcation Repriced the AI Compute Stack — Documents the compute-stack repricing that made power, rather than chips, the next binding constraint.

Energy, Infrastructure, and the Grid

The Power Stack: How Energy Infrastructure Became the New AI Battleground — Forecast the trigger conditions for government intervention that EO 62 satisfied; Section I scores the resolution.

The AI Infrastructure Energy Opportunity Landscape — Supplies the constraint-removal versus choke-point distinction and the Geodesic Availability Ratio test applied in Sections V and XI, and forecast the state-by-state permitting divergence documented in Sections VI and VII.

The AI Infrastructure Energy Antitrust Landscape — Maps the enforcement exposure that Section V’s self-reinforcing loop predicts moratorium windfalls will attract.

Chevron–Microsoft Project Kilby and the Firm-Power Forecast — Documents jurisdiction selection as a regulatory routing layer; the ERCOT precedent behind Sections IV, VII, IX, and X.

The Federal-State AI Infrastructure Collision — Forecast partial federalization, the coordination tax, and New York’s conditioning posture; Section VII tracks each against the FERC §206 proceeding.

The DOJ–FTC Gas-Price Letter to State Attorneys General — Establishes the federal energy-market intervention posture that frames the enforcement trajectory in Sections V and X.

Method Frameworks

Predictive Game Theory Meets the Era of AI — Operationalizing Fudenberg’s Research Agenda with Cognitive Digital Twins — Supplies the game-replacement framework and Adaptive Coherence Equilibrium concept applied to the actor field in Section IX.

The MindCast AI Dynamic Predictive Game Theory Collection — Collects the foundational game-theory pieces behind the Section IX analysis in one visual edition.

Synthesis in National Innovation Behavioral Economics and Strategic Behavioral Coordination — Quantifies institutional throughput: the five-to-one temporal mismatch in Section VII, the reviewer loss-aversion finding in Section IX, and the Washington seven-layer analysis in Section XI.

White House Genesis Mission x NIBE — Demonstrates that correcting mid-level reviewer incentives outperforms senior oversight, the finding that gives plank three its mechanism.

Law and Governance

The Commerce Clause as America’s AI Advantage — Establishes the constitutional path for federal AI infrastructure coherence and the absorption model behind Section VII and prediction AIRC-III-13.

Susquehanna Is Building the Institutional Market the CFTC Does Not Require — but Still Needs — Documents the parallel legitimacy game: building the record a regulator politically needs before the law requires it, the same structure as New York’s grid-fund exit.

Academic Foundation

Kahneman, D., & Tversky, A. (1979). “Prospect Theory: An Analysis of Decision under Risk.” Econometrica47(2): 263–291 — The loss-aversion mechanics applied at the community, gubernatorial, and reviewer levels in Section IX.